The Prime Minister has just announced his resignation. A Conservative MP who voted to leave said we must remember that nothing will change.

Everything will change and in ways which we cannot predict we cannot know what we cannot know.

The economy is characterised by positive feedback. This means a small change in one part of the system is magnified by the systemic response. As I write this, global stock markets are crashing, sterling has fallen to $1.30, and Moody’s have said the UK will lose its AAA rating. These are knee jerk reactions but they are destabilising: positive feedback has already been triggered. The Bank of England has made soothing noises and will supply short run liquidity to prevent the wholesale market from seizing up.

Boardrooms round the world will be trying to evaluate both the risks and the opportunities. Everything will change, and it has already started.

Some background.

Since the early 80s, skilled and semi-skilled workers in the USA, the EU and the UK have experienced falling real incomes. The share of national added value going to capital has increased (this means shareholders). This increase in inequality is now being reflected

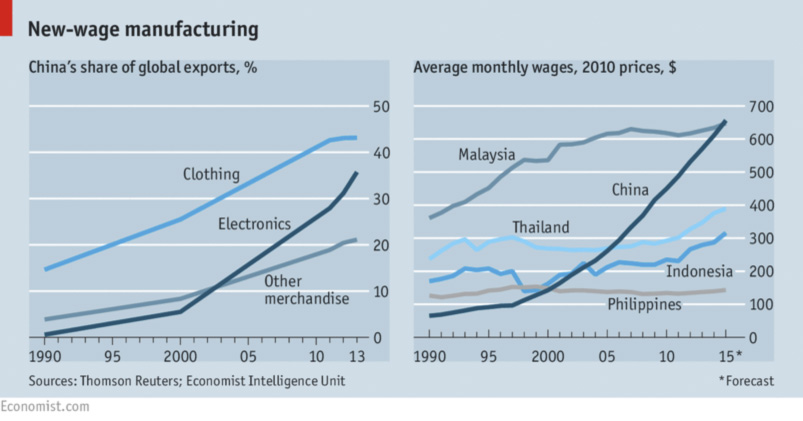

at the ballot box. The voters think it is caused by the political class, and in the UK by immigrants from the EU. This is incorrect. It is China. From 1980, 1.2bn new workers joined the global economy and this depressed real wage growth. At the same time shareholders approved reward schemes for senior managers based on earnings per share growth which prompted outsourcing, labour saving technologies, and headcount reductions.

Taken in combination the result has been a significant increase in income inequality in the West and the voter has reacted to it. This is why we have Trump, Brexit, the rise of the extreme right in the EU and significant mistrust of institutions.

The entry of China into the global system has driven the West to move further up the added value chain which has increased the demand for highly skilled employees, and reduced the demand for the unskilled (and their real wages).

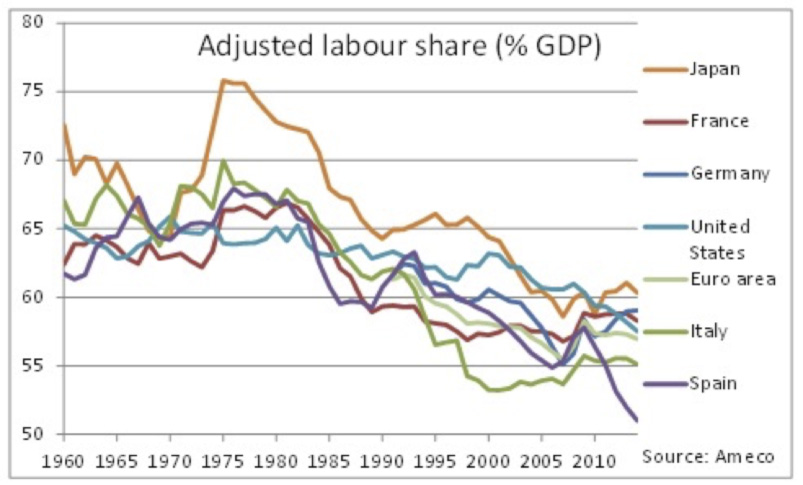

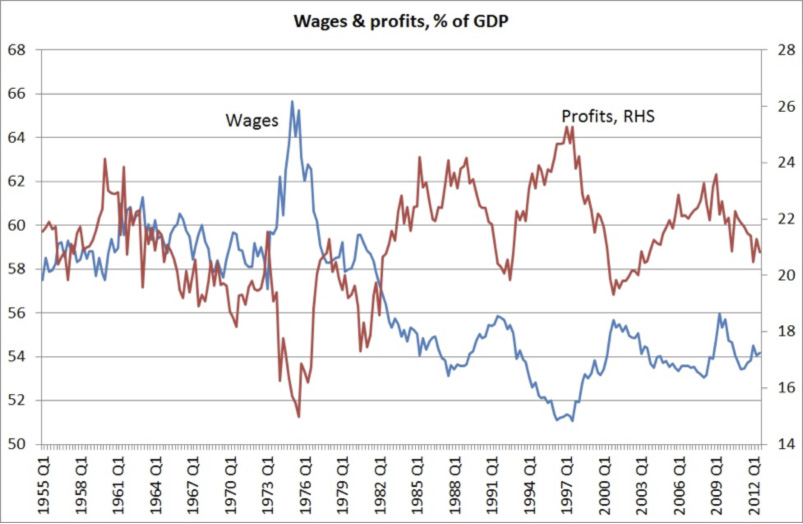

The chart above shows the data for the UK. Prior to 1982 wages were around 59% of GDP, since then they have averaged 54% of GDP. And the share of profits has increased.

It is my opinion that these fundamentals are now driving the attitude of the electorate who tend to sum it up in simple terms: blame it on immigrants, the ruling elite and the unelected bureaucrats in Brussels who are depressing wages.

Brexit does not change this at all. It is not the solution. The solution is a significant increase in the education and training of those who have suffered falling real wages.

What is the outlook?

History tells us that the perceived value of property is a significant driver of consumer confidence. The mortgage rate is closely aligned to the yield on Government bonds. The yield depends on expected movements in the exchange rate, the Government’s budget position, political risk and expected inflation.

If we lose our AAA rating, the yield on bonds could rise, but a weaker sterling could offset this. However, if a further weakening is expected, then overseas purchasers will wait and the Government will have to raise the interest rate or cut the price in order to obtain finance. Either way the cost of financing our £1.56 trillion national debt will rise. It costs 43Bn a year at present. The Bank of England could do more QE but I doubt it.

As a rough rule of thumb, every 10% fall in sterling adds 1% to CPI within a year (unless offset by price cuts from China).

We have a deficit on our balance of payments equal to 7% of nominal GDP, this has to be financed and higher interest rates enable this.

Over the next three years we can forecast interest rates higher than expected, house prices stagnating or falling, inflation higher than expected (real incomes falling), consumer spending dropping from 4% year on year to 1-2%. Real growth falls from 2.5% per annum to under 1%. Unemployment begins to rise in a year, net migration drops to around 140,000.

Government income falls below plan and either borrowing goes up (currently £68Bn a year) or the rate of growth Government spending has to fall.

There will be a new PM in the autumn. He or she will write the letter to leave the EU or conceivably he or she might wait to see the results of elections in Germany, France, Czech Republic, and Hungary.

Existing trading agreements will remain in place which will give the UK time to build a team of negotiators (it will cost a fortune, we will have to poach them from Brussels!)

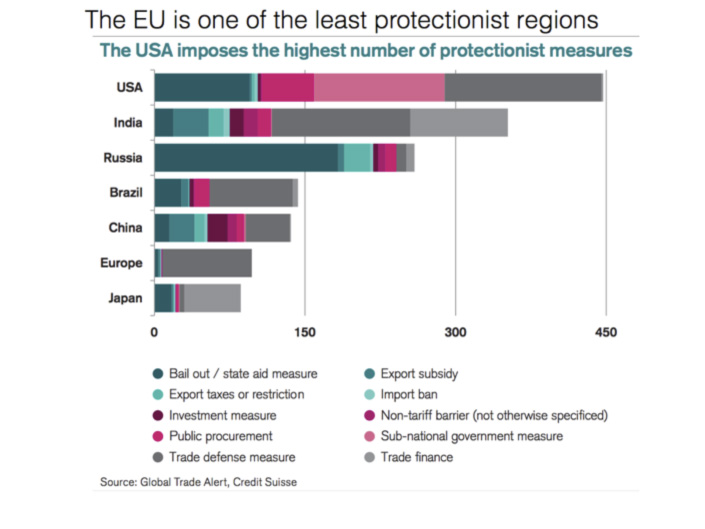

The EU is one of the least protectionist regions (see chart on the next page) and that is where we should place all our efforts. However, a free trade deal will require free movement of people.

Meanwhile the political risk in the UK will trash investment spending particularly from overseas. This impacts on longer run productivity growth.

I have not made any numerical forecasts because it is too early to have a view. I can be confident that we should expect much lower growth than forecast at the beginning of the year. We are unlikely to have a clear view until we know who our leader is.

I note that Sunderland were overwhelmingly in favour of leaving. Nissan employs 9000 people. The £100m investment for the Nuke car may be cancelled. Nissan will face a 10% tariff on sales to the EU once we leave. There is naught so queer as folk!

I suspect there are many who voted leave, with no expectation that it would actually happen, they just wanted to give the toffs a bloody nose. Regrettably it will be the working poor who will get the bloody nose over the next few years.

My personal view is this event will prove to be a mistake. It is companies who trade with each other, not governments. I cannot see how the vote will change the desire of companies in the UK to seek overseas markets with more vigour. The EU will still be our biggest market and as it recovers strongly over the next few years, we may regret leaving the table.

Rushed out on June 24 2016

Roger Martin-Fagg