The latest economic update from one of the best economic forecasters in the UK, Roger Martin Fagg.

The latest economic update from one of the best economic forecasters in the UK, Roger Martin Fagg.

Many of Property Academy’s Members have had the experience of working directly with Roger in our mastermind group meetings and all our members receive his regular economic briefings.

Roger called the last shock General Election result and accurately predicted that Trump would be President months before anyone else. You can find more information about Roger, the many other benefits of Property Academy membership and apply to attend a Mastermind Group session at the bottom of this update.

In addition to his usual summary of world events, in this update, Roger writes a very honest personal ‘school report’ – comparing his recent predictions against actual performance. He may not always be right, but in the words of famous British Economist John Maynard Keynes, “It’s better to be roughly right than precisely wrong” and Roger is certainly top of his class.

I have had to rewrite this update twice with no thanks to our Prime Minister. No doubt by the time you come to read it,events will have rendered some of it irrelevant.

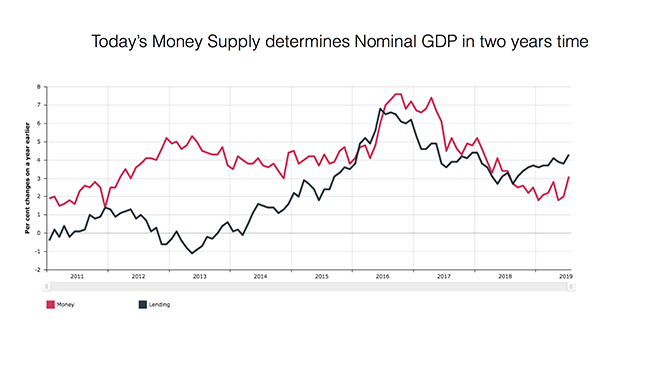

The UK money supply

Money supply growth has been half the rate we need for 2% real growth rate.

The effect is now beginning to come through after the usual time lag.

Employment has peaked, albeit at a record level. We will not see unemployment rising until the fourth quarter of this year, but it will. The current strong growth in earnings (4% year-on-year) reflects the high rate of money supply growth in 2016 and 2017. The lower money supply growth which began a year ago will impact in Q4 of this year. There is a faint chink of light, as money supply for August grew by 3%.If this is maintained and we get a transition deal done, a recession will be avoided.

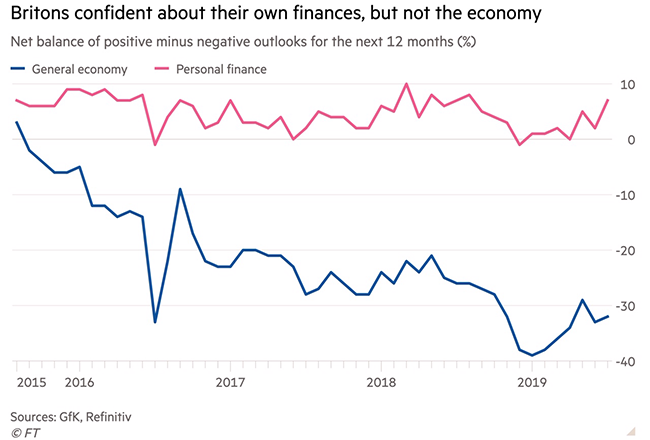

The growth in earnings, plus stable house prices, has created a sense of ‘all is well’ for the average person in the street. It is a paradox – people think the economy will worsen but their own situation will not. My view is so long as house prices do not fall, and unemployment doesn’t increase,people will continue to think their financial position is fine. Additionally many will have the view that a hard Brexit may create a short recession but then growth will resume at a faster rate as the UK forges new trade deals round the world. It is worth noting, though, that Trump has signed zero trade deals. And post Brexit we still have 708 trading agreements to carry over or renegotiate. In the past three years we have agreed 42 of these.

Back to politics: the election window is November 2019, any later and the data will be going the wrong way.

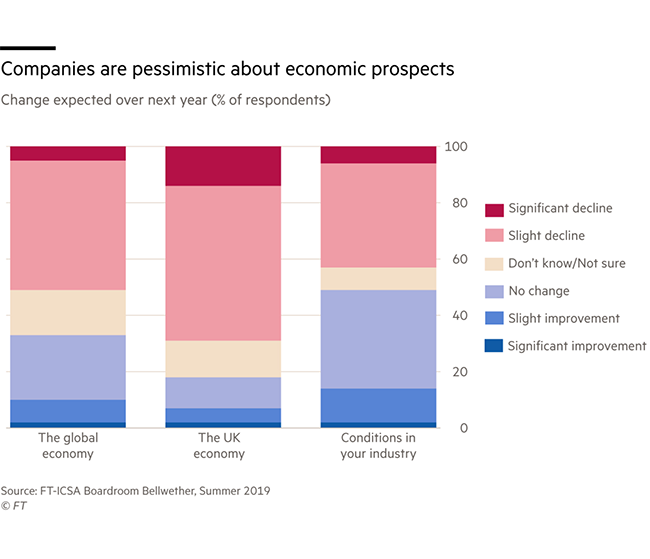

Below is the latest survey from UK Boardrooms.

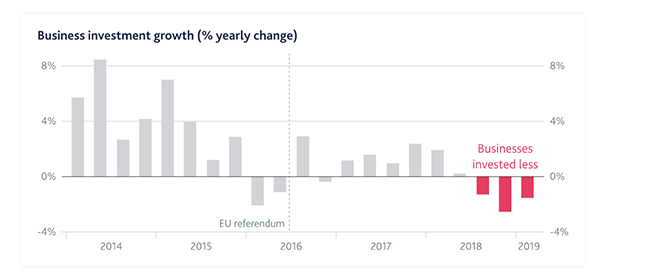

The consequence of uncertainty is less investment spending which has a direct impact on competitiveness and future productivity.

There is widely held view that the devaluation of sterling since the referendum boosted UK exports. Sadly, this is not the case. But it does make UK assets cheap for overseas buyers and this enables us to run the largest balance of payments deficit of the G20 group. After October 31st sterling will fall further if there is no deal.

I guess it will reach $1.15 and €1.05. This fall is essential to ensure foreigners buy the UK at bargain prices.

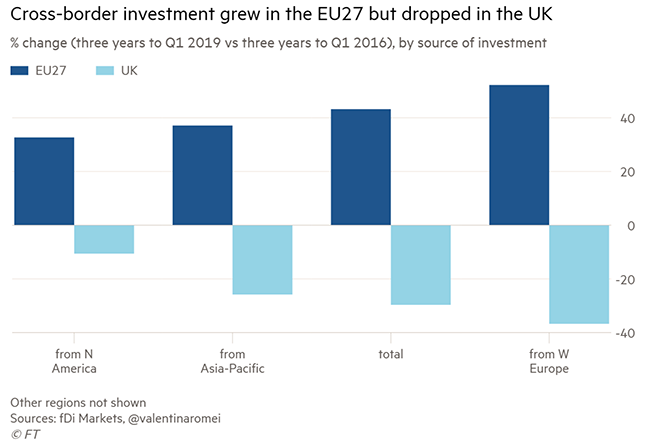

Unfortunately the UK is now losing the stable inward investment which has financed our trade deficit since the mid-1980s, and which has been a major contributor to our productivity growth.

Combine this with domestic investment and it presents bleak picture. It is very difficult to view Brexit as anything other than an act of self-harm.

I was once introduced as the economist who predicted seven out of the last three recessions. Not true but I state this because I could be wrong. If the data changes so will my opinion. But my current view is we will be close to recession in Q4 2019. And if we have a no deal Brexit a recession.

Will it be deep or shallow? It is clear that our banking system is well capitalised and will not suddenly seize up as happened in Q3/4 2008. This will prevent a collapse in house prices which in the last 30 years has been the driver of deeper recessions. The inevitable supply chain disruption will create some shortages and delays to both exports and imports. How long this persists will depend on negotiations with the EU (in my opinion we will be on the back foot) because their economies will not suffer to the same extent.

My guess is UK real GDP will drop between 2 and 3% with a no deal Brexit when comparing Q4 2019 with Q4 2020. If there is a managed exit with a transition period then I guess no growth compared to a year earlier but we will avoid recession.

There are two key variables: the volume of money and how many times it gets spent.

The velocity of money has been falling since 1971 because banks have been creating so much of it. In 2010 Banks stopped creating money. Velocity stopped falling and then began to rise, until banks began creating money again in 2015.

The depth of a UK recession will depend both on the banks and household confidence, which in turn will depend on house prices and the growth in real wages. My forecast of a drop 2 – 3% in real GDP with a no deal Brexit assumes that both money growth and its velocity fall for a year or so. It also assumes a weaker pound pushing up domestic prices faster than income growth, thus reducing real incomes.

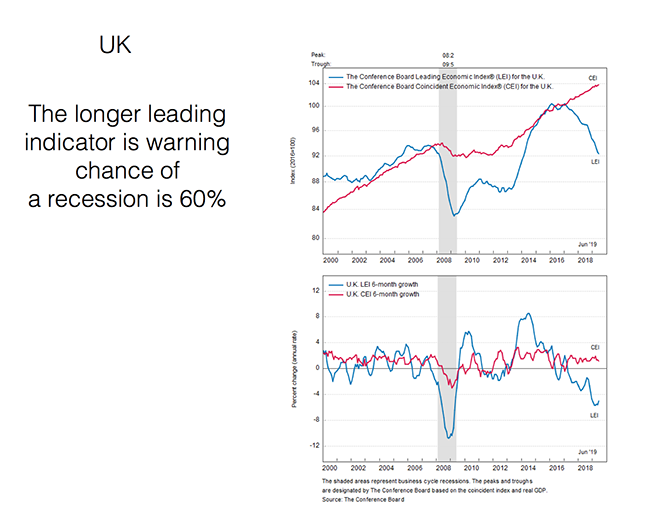

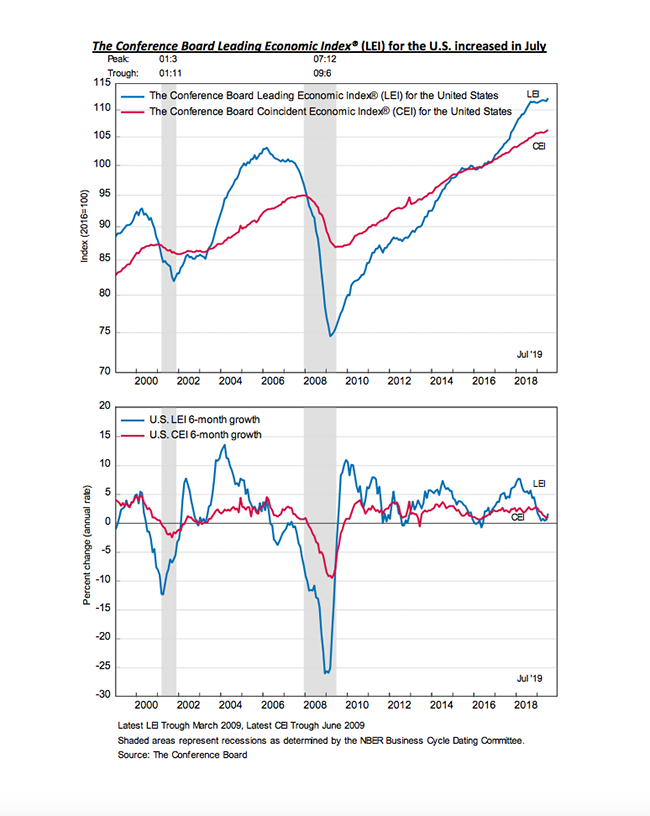

The Independent Conference Board in the USA uses an index of 9 time series to look forward.

Here is their latest opinion.

What can a business owner manager do about this?

As a behavioural economist I emphasise the fact that people behave instinctively for 80% of the time.

If your business is experiencing difficult times then your leadership becomes more important than ever. The research is clear: people who exercise power over others tend to be more self-centred and less mindful of the needs of others. They also act as if custom and practice norms of behaviour do not apply to them. Furthermore they believe they are aware of everything that goes on in their business. (Observe our Prime Minister!)

Meanwhile employees devote much time to interpreting every nuance of the boss’ behaviour, looking

for signs which may indicate what will happen to them.

Employees have four, often unmet, needs.

Predictability, understanding, control and compassion.

Predictability is about what will happen to my career with the company, understanding is about why and how. In a recession things change. Employees need full information as to why and in what way. The leader needs to give information which is simple, concrete and most important of all, repetitive. The employee needs to be able to read the body language: emails and videos do not work. It has to be face to face.

It is important that people who are affected by the change are given control of how to proceed.

Change is complex, but it can broken down into small discreet actions which people will take if it is in their control.

Compassion can and does take many forms. At its heart it is as simple as adopting the other person’s point of view, understanding his or her anxiety, and making a sincere effort to soothe it. Research shows that compassion at its best allows individuals to retain their dignity.

As economic conditions deteriorate, employees will need frank and honest communication. It is amazing what people can achieve if the challenge is clearly defined and control is passed to them.

Here is my list of the five key actions.

- Reduce company debt

- Define market positioning, distinctiveness, and what makes you compelling

- Increase the amount of face to face communication with everybody

- Ask employees to look at ways of enhancing business performance: the opportunity cost of digitisation is lower when customer demand is smaller

- Automate, particularly back office activities

If cash is tight, limit wage awards but increase the bonus pot for future distribution (and make sure employees know this!)

In the last recession many UK owner managers increased their investment (and reduced dividends), they reorganised, they digitised and they flourished. Many of those who didn’t are no longer trading.

The Rest of the World

As the chart below shows the US treasury bond yield curve inversion historically has been a predictor of recession. The curve suggests that investors prefer bonds to other assets (because they are safer) and also suggests that central banks will cut interest rates. As you can see from the chart there is a variable time lag. And this data must be viewed in conjunction with other data. But historically the US stock market has collapsed 18 months after yield inversion.

The Longer Leading Indicator is still positive for the USA (but it doesn’t look beyond a year)

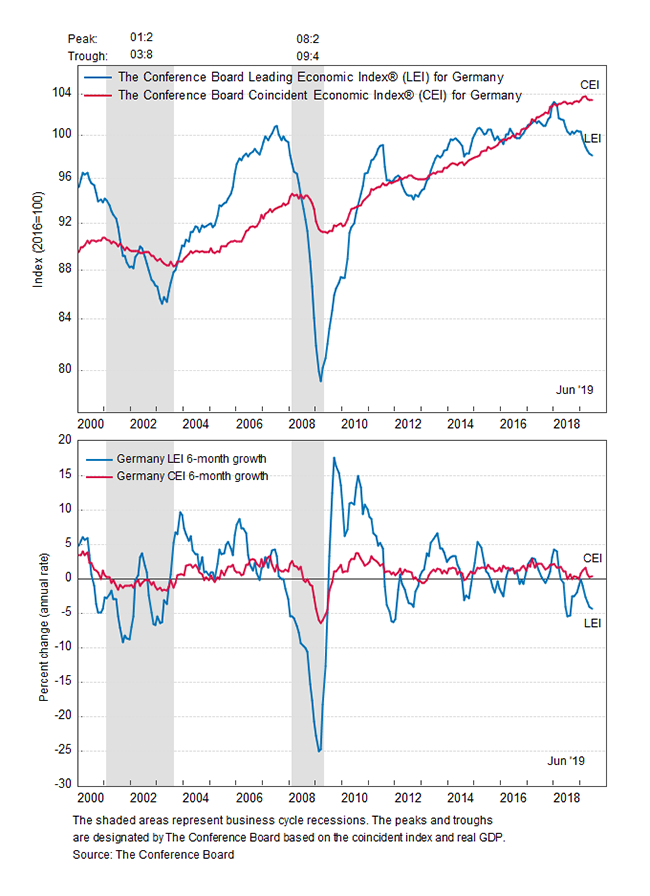

Germany

Germany is suffering from slower international trade and Brexit.

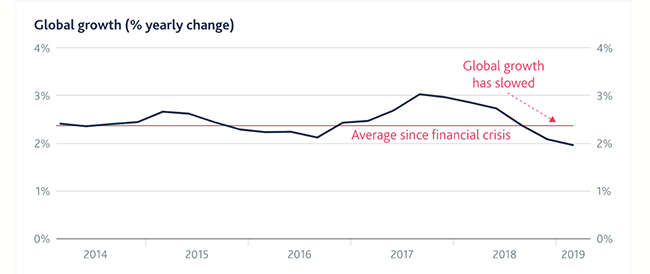

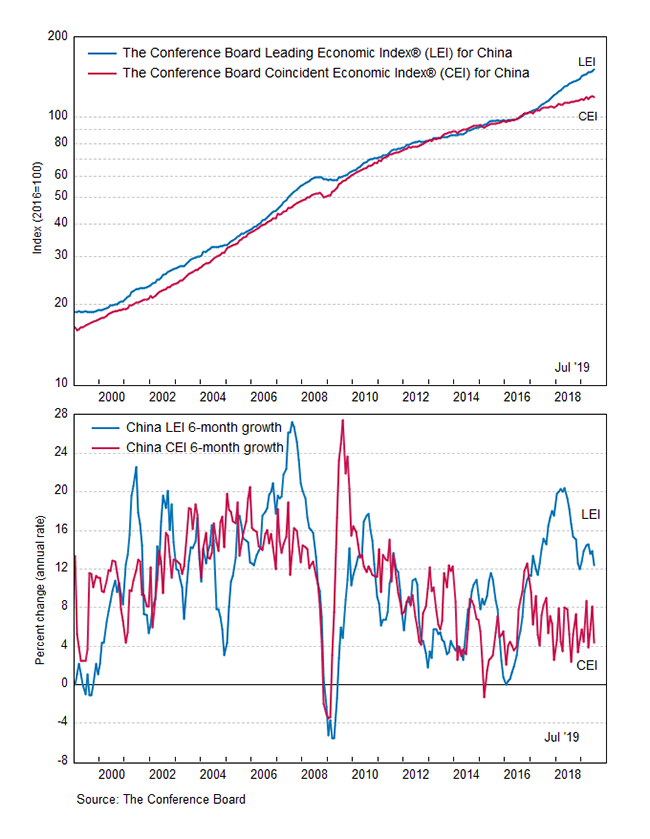

China is growing as usual. The trade war with the USA has reduced its growth rate by around 0.2%. The dispute is more about who runs the world over the next 30 years.

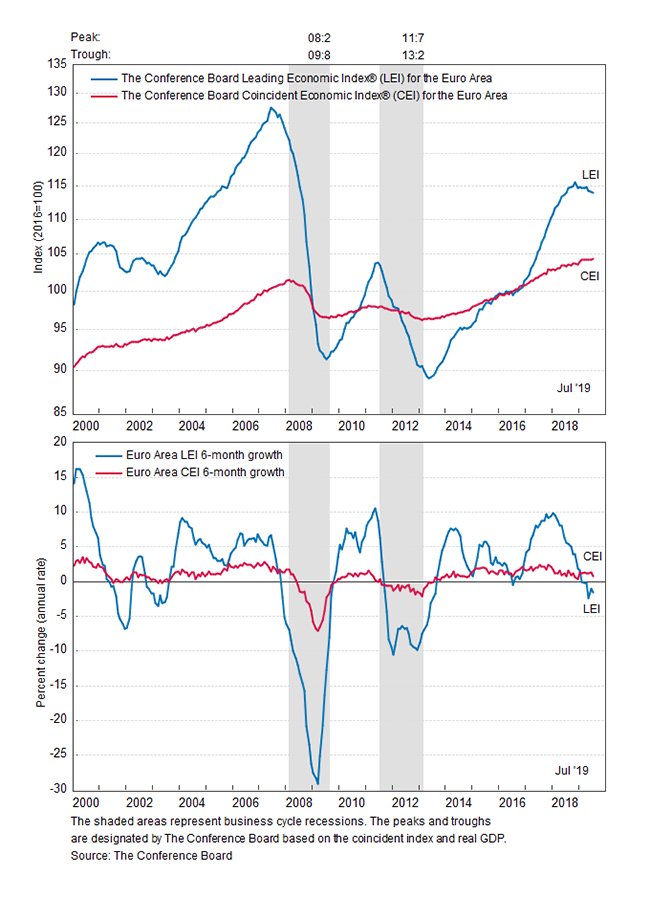

And finally the Eurozone as a whole (includes Germany which is a third)

This update was finished at 4pm on September 11 2019. I know that by 6.30 pm things will have changed as populist leaders utter more soundbites to continue their assumed path to greatness.

Rmfagg@aol.com September 2019

Roger Martin-Fagg

Roger Martin-Fagg

Roger Martin-Fagg is an economist turned strategist.

A behavioural economist who focuses on behaviour and feedback loops which are largely absent from conventional models.

He began his career in the New Zealand Treasury, then moved into Airline Business Planning and teaching postgraduates all aspects of economics. He designed and ran the postgraduate diploma in Airline Management for British Airways before joining Henley Management College in 1987, where for 21 years he taught senior managers macroeconomics and strategy.

Roger is an independent teaching consultant. He has been external examiner to Bath University, worked with the Bank of England, three of the major UK clearing banks, advised a major London recording studio for 15 years, and regularly talks to SME owners in the UK and Europe about economic trends. He is a visiting fellow to Ashridge, Warwick and Henley business schools.

Roger is a practical researcher. He focuses on how the economy really works and on the links between FT100 reward systems, the behaviour of banks and economic instability. He also researches his clients trading environment as a necessary component of his teaching. His book

“Making Sense of the Economy” is in its fourth reprint.

He speaks at conferences around the world on the economic outlook and its impact on business. His quarterly Economic Update is sent to 1,200 SMEs.

Roger is one of over 70 experts that works with the Property Academy’s members. Want to find out more about the benefits of Property Academy membership and attend a free trial meeting?

Follow our social channels here: