The latest economic update from one of the best economic forecasters in the UK, Roger Martin Fagg.

The latest economic update from one of the best economic forecasters in the UK, Roger Martin Fagg.

Many of Property Academy’s Members have had the experience of working directly with Roger in our mastermind group meetings and all our members receive his regular economic briefings.

Roger called the last shock General Election result and accurately predicted that Trump would be President months before anyone else. You can find more information about Roger, the many other benefits of Property Academy membership and apply to attend a Mastermind Group session at the bottom of this update.

In addition to his usual summary of world events, in this update, Roger writes a very honest personal ‘school report’ – comparing his recent predictions against actual performance. He may not always be right, but in the words of famous British Economist John Maynard Keynes, “It’s better to be roughly right than precisely wrong” and Roger is certainly top of his class.

As I write this there is no clarity from Westminster on how the UK with withdraw from the EU if at all. The uncertainty is weighing heavily on UK investment spending and the velocity of money. UK business is holding onto cash. A recent survey indicated that around £750Bn is currently sitting in cash in UK company balance sheets. This is a record. And it means a third of the UK money supply is not flowing through our economy financing investment in automation, training, equipment and innovation. From the individual company perspective it is prudent, from a system perspective it is damaging.

Additionally the quantity of money in our economy is growing at half the rate required to produce a GDP real growth rate of 2.3%.

In combination it is difficult to be optimistic about the next 18 months. The good news is the Brexit timetable suggests a decision by the end of October. And following a decision one would hope that a good chunk of the £750 Bn would be spent. If so we will avoid recession and may have a growth burst. The so called Brexit dividend.

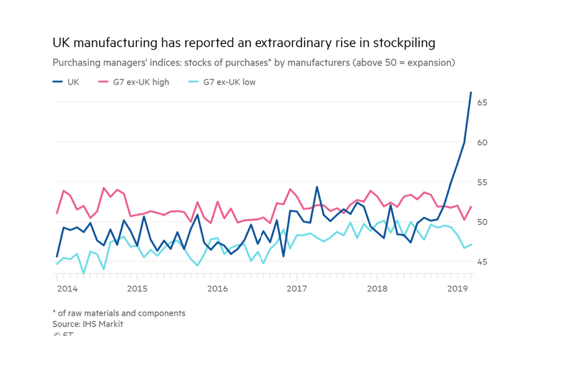

But look at the chart. Stockbuilding boosts intermediate demand but not final demand. The stock-build is a sensible response by individual companies to possible supply chain disruption. But if the withdrawal deal goes through, then for at least two years and probably three, the UK economically remains part of the EU. Unless final demand increases substantially, destocking will take place and cause a manufacturing recession. A paradox: we have a decision on the EU and we get a mini-recession! Of course if we leave on WTO terms then the subsequent supply chain disruption will have a reduced impact due to accumulated stock in our system.

The latest data on investment spending is shown below: Brexit uncertainty is clearly having an impact.

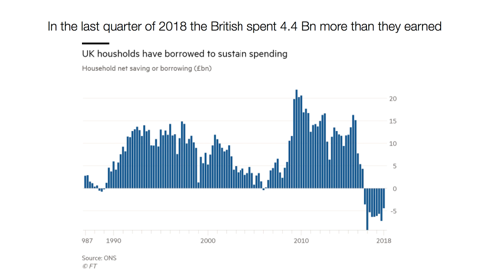

Retail sales picked up in April. But the data for the last quarter of 2018 shows that households are still using debt to maintain their lifestyle (and in some cases survive). As the chart shows this has not happened to same degree before. If there is a Brexit dividend then high levels of employment plus real wage growth of 2% will allow indebted households to survive. But if not, then we can expect a significant increase in personal bankruptcies.

UK Retail Sales mom

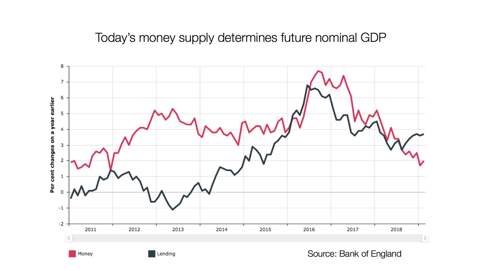

However the big elephant in the room is money supply. As I have said before the UK needs money growth of 4-5% per annum to enable real growth of 2-2.5% with an inflation rate at the target level of 2%.

The chart shows March money supply at 2% growth. Unless this picks up back to 4% we can look forward to a tough 18 months with the UK economy close to recession.

There is some good news. The price of oil is sitting around $62 a barrel. Although UK household utility bills are beginning to reflect last summer’s hike. OPEC have a target price of $70 for the end of 2019 but non OPEC member pump rate might render that unachievable.

The price of oil in US dollars

UK house prices.

It is now well understood that the perceived value of property is the major driver of confidence for bankers and property owning households. There are now significant regional differences. The South has stalled with no price increase in March, but all other regions show growth of between 2 and 5%. I do not think this is a consequence of Brexit. It is because at last the South is showing the long overdue price correction. The sustainable long run average % of after tax income spent on mortgage finance is 33%.

Clearly property in London and the South East is overpriced. And so the price correction should continue until falling prices meet rising incomes. This is not a problem for the average house purchaser who stays in their current house of 7 years. But it may catch out the leveraged speculator ( and their bank!)

The Global Economy

Last July I suggested that the global economy was at the top of the cycle. The data since then supports this view. The key question is will we experience more slow down but no recession or a rapid descent into recession.

The effect of the Chinese/ Trump tariff war has reduced trade volumes between them but not by much and the USA is the loser. Exports from the USA to China are down by 30%, but from China to the USA by just 2.8%. And the effect is mitigated domestically by tax cuts in the USA and monetary stimulus in China. China will grow by 6.7% and the USA by 2.3% (the constraint on USA growth is currently labour supply).

The EU

In recent months Germany has seen a significant slow down in manufacturing due to softer demand for exports. But domestic demand is taking up some of the slack and Germany will grow at 1% this year.

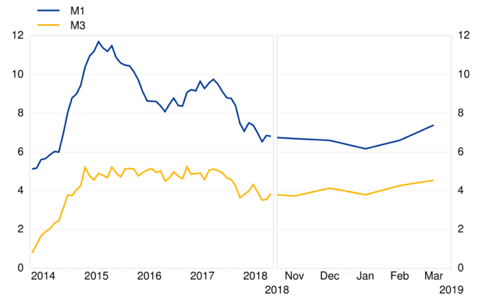

The money supply data suggests the EU as a whole will avoid recession. In the chart M3 is the EU equivalent of the UK M4. You will recall UK money supply needs to grow at 4% but is only growing at 2%. M1 measures the growth in current account balances.

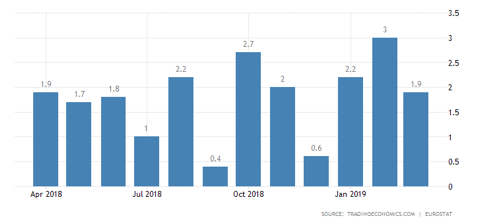

Monetary conditions are just fine in the EU; the question is what will happen to confidence and velocity of money.The retail sales data shown below show a steady performance. Although consumer confidence data indicates a softening.

I have to say that if someone gets their view of the EU economy from the Telegraph they would have a much more pessimistic view. But such is the quality and bias of British journalism. In the interests of objective analysis I show below the view of economists in the USA.

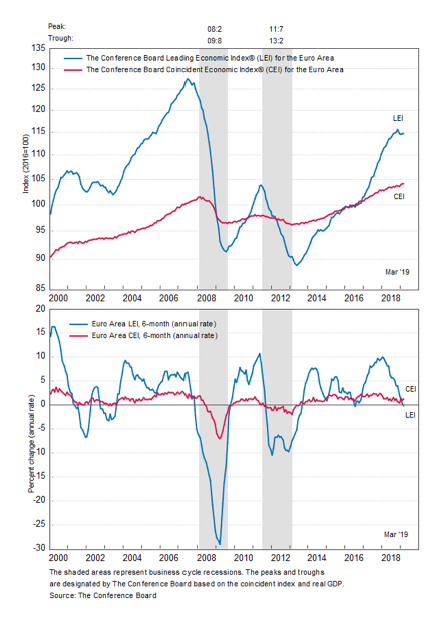

The chart is for the EU.

The Longer Leading Indicator is a composite index composed of 7 time series it looks ahead for about a year. The Coincident Indicator is the cycle itself. The chart suggests that over the next year the EU will grow but at a lower rate.

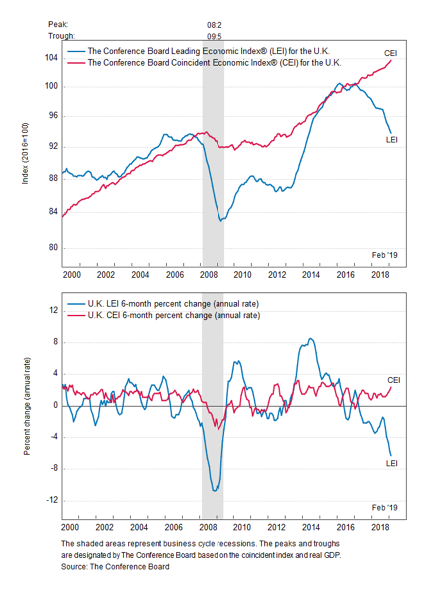

Now we look at the same indicators for the UK. Note the chart says Feb19 but the data is for March19. They suggest the UK will be close to or in recession a year from now. This is consistent with the money supply data (which is not one of the 7 time time series).

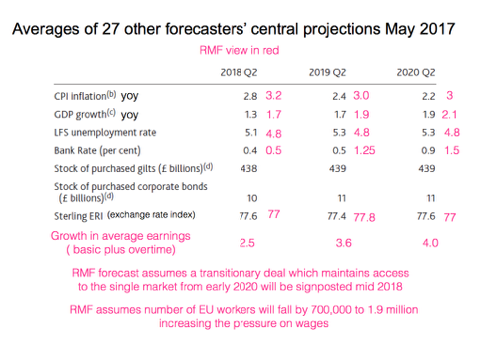

Now for the school report.

Here are the forecasts I made two years ago.

CPI inflation for Q2 is expected to be 2%, my forecast of 3 clearly incorrect.

GDP growth for Q2 is expected to be 1.3% my forecast of 1.9 again wrong Unemployment rate is 3.6%, I forecast 4.8%Bank rate 0.75% I forecast 1.25%

Exchange rate index 77.5 I forecast 77.8

Growth in average earnings 3.4 I forecast 3.6%

I assumed a deal would be done by now Ha!

Number of eu workers has only fallen by 268,000

What follows is a direct quote from my school report aged 13.

Martin-Fagg is not bottom of the class this year because of a new boy who arrived recently

So it would seem nothing has changed!

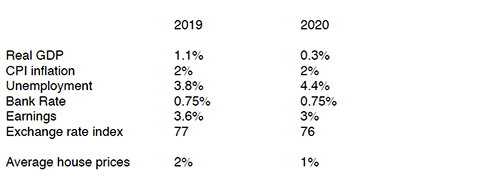

Here are my forecasts for the next two years

On Brexit I have no idea!

As individuals we cannot control national or international events. We should only worry about that which we can control which is our attitude to others. At a time of political turmoil we should always respect the opinion of others even if we fundamentally disagree. Over the next two years the potential for significant societal unrest will exist. We should ensure a balanced, and measured response to others. And avoid posting tweets, emails and other social media which have not been carefully thought through as to how the wording might be interpreted.

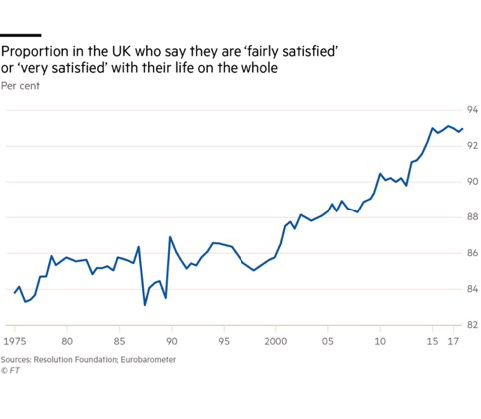

Despite everything a recent survey shows that 93% of the British are fairly or very satisfied with their life on the whole (see below). Long may it continue.

Rmfagg@aol.com May 2019

Roger Martin-Fagg

Roger Martin-Fagg

Roger Martin-Fagg is an economist turned strategist.

A behavioural economist who focuses on behaviour and feedback loops which are largely absent from conventional models.

He began his career in the New Zealand Treasury, then moved into Airline Business Planning and teaching postgraduates all aspects of economics. He designed and ran the postgraduate diploma in Airline Management for British Airways before joining Henley Management College in 1987, where for 21 years he taught senior managers macroeconomics and strategy.

Roger is an independent teaching consultant. He has been external examiner to Bath University, worked with the Bank of England, three of the major UK clearing banks, advised a major London recording studio for 15 years, and regularly talks to SME owners in the UK and Europe about economic trends. He is a visiting fellow to Ashridge, Warwick and Henley business schools.

Roger is a practical researcher. He focuses on how the economy really works and on the links between FT100 reward systems, the behaviour of banks and economic instability. He also researches his clients trading environment as a necessary component of his teaching. His book

“Making Sense of the Economy” is in its fourth reprint.

He speaks at conferences around the world on the economic outlook and its impact on business. His quarterly Economic Update is sent to 1,200 SMEs.

Roger is one of over 70 experts that works with the Property Academy’s members. Want to find out more about the benefits of Property Academy membership and attend a free trial meeting?

Follow our social channels here: