The latest economic update from one of the best economic forecasters in the UK, Roger Martin Fagg.

The latest economic update from one of the best economic forecasters in the UK, Roger Martin Fagg.

Many of Property Academy’s Members have had the experience of working directly with Roger in our mastermind group meetings and all our members receive his regular economic briefings.

Roger called the last shock General Election result and accurately predicted that Trump would be President months before anyone else. You can find more information about Roger, the many other benefits of Property Academy membership and apply to attend a Mastermind Group session at the bottom of this update.

In addition to his usual summary of world events, in this update, Roger writes a very honest personal ‘school report’ – comparing his recent predictions against actual performance. He may not always be right, but in the words of famous British Economist John Maynard Keynes, “It’s better to be roughly right than precisely wrong” and Roger is certainly top of his class.

WHAT STAGE OF THE ECONOMIC CYCLE IS THE UK IN?

A cursory glance at this chart would suggest the latest cycle began in 2010. The typical cycle is 7-9 years long, so we can forecast the UK is close to a cyclical peak. It is also possible to argue that the recovery was so weak until 2013 that this peak may not be reached until 2020 or 2021.

The first quarter of 2018 has been weak for both the UK and the EU. The beast from the east storm probably halved the quarterly growth rate to around 0.2%, so we must discount this weather determined data and look at the trend.

Let’s look at the characteristics of a cyclical peak

The labour market tightens with wages growing faster than productivity so that either profit margins are eroded or inflation increases. Currently, UK wages are growing at 2.8% inflation is 2.5% productivity growth is 0.8% and unemployment is 4.4%. This data supports the tight labour market observation.

Long run interest rates begin to rise due to heightened inflationary expectations. The 15 year gilt yield was 1.4% a year ago. It is now 1.7%. Not a dramatic increase, but on the way up.

Commercial property yields fall. This is because rising demand boosts capital values but not rental prices, which are usually fixed for a number of years. This is happening for both primary and secondary property. Prime yield has fallen from 7% in 2009 to 4% now, and secondary yield from 11% to 8% over the same period.

P/E multiple for shares rises above long run trend. Here the evidence is mixed. The FT250 P/E is 19 which suggests that shares are priced at long run trend. The FT100 is best ignored because the exchange rate and not the UK is the main driver of share prices. Overall UK equities are not overpriced.

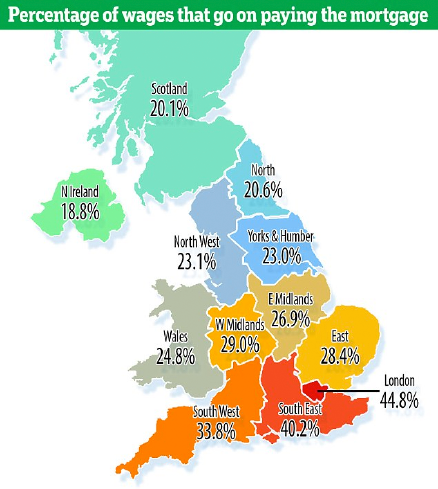

Housing becomes unaffordable near the top of the cycle. Contrary to popular belief UK houses are more affordable today than they have been for the last 10 years. Last year UK households spent 29% of their after tax income on mortgage costs. In 2007 it was 48% and in 1996 (when house prices had been falling for 5 years) it was 23%. Please note the chart above refers to after tax wages. London and the SE are always the exception.

The affordability index today is below 1984-1991 and 2004-2009. This is because money is cheap. However the Bank of England will raise rates this year. Bear in mind that dearer money does not mean reduced affordability if wages are rising faster than interest rates, which can be expected.

The Government announces the budget deficit has dropped faster than forecast and claims economic competence. The charts shows that for most of the last year some of the national debt has been paid down.

Overall my view is that we will reach the top of the cycle over the next 12 months. But, because Brexit has increased uncertainty, reduced capacity creation, and trashed household real incomes, the top is much less frothy than is typical. Therefore the slowdown should be gradual rather than sharp. And it should last the typical 2 years. That is assuming a soft Brexit with no major trade disruption.

Most of my readers are SME owners. The best indicator of an impending downturn is large companies failing to pay your invoice on time with a list of pathetic excuses!

THE FUTURE PATH OF INTEREST RATES

The monetary policy committee have to look ahead two years and guess how the economy will be performing. Their remit is to ensure CPI inflation is 2% whilst taking broader economic considerations into account. They accept that the UK is currently running at capacity but are surprised that wage inflation remains relatively subdued. The latest money and credit data suggest that there is sufficient monetary expansion to enable 3% wage inflation. Productivity growth suggests an inflation rate much closer to 3% than 2%. So interest rates have to be increased to moderate the demand for credit and thus the growth in the money supply.

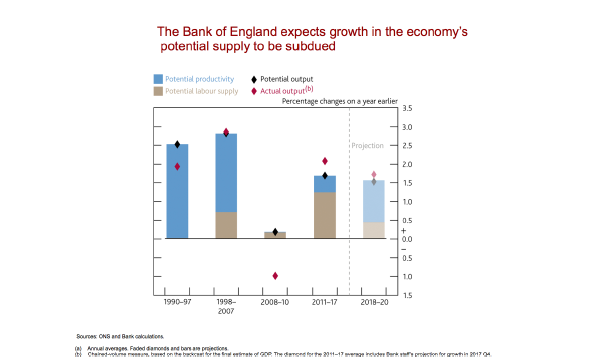

Remember when a bank makes a loan it simultaneously creates money. The money supply data for March shows a slow-down in the growth of lending and money supply, possibly due to the weather. Based on this data the MPC will delay increasing interest rates until they are clear of the trend. The chart on the next page will be a guide to the Bank’s thinking.

The chart shows that the UK full employment growth rate has dropped from 2.5% pa to 1.5% pa. These estimates could be wrong, but they will be a deciding factor on the path of interest rates. Lower growth potential requires lower money supply growth, which requires higher interest rates.

THE RMF SCHOOL REPORT FOR 2017

Here are the guesses I made a year ago.

Here is the latest data:

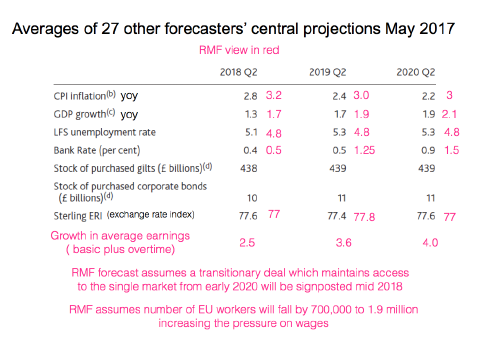

Inflation: CPI 2.5%, CPIH 2.3% and RPI 3.3%.So a fail on this.

GDP growth: data not available until June but likely to be 1.5% due to weather. So probably will get this wrong.

Unemployment rate: 4.2%, forecast was 4.8%, again wrong.

Bank rate: 0.5% CORRECT

Effective exchange rate index: 80, forecast of 77 – wrong.

Growth in average earnings 2.7%. I forecast 2.5% – close, wrong.

Transitionary deal has been agreed. CORRECT

Reduction in EU workers 100,000k so far- I may get this one right in time.

Overall score 2 out of 8. But the average of 27 forecasters: all wrong!

Headmaster’s comment:

RMF has performed better than the average for the class of 27 who produced an appalling result. This is no achievement. We continue to live on in hope of better results.

THE REST OF THE WORLD

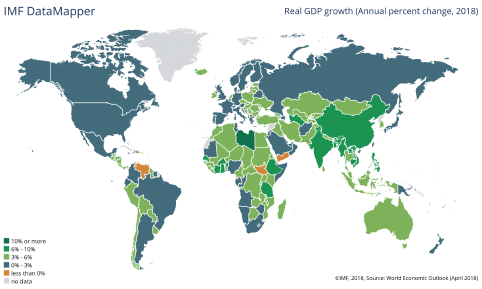

It continues to expand faster than forecast (but we already know that forecasters get things mostly wrong!). It is driven by the USA, China and the EU in that order.

There are only three countries which are not growing. The Yemen, South Sudan and Venezuela.

WHAT ARE THE RISKS?

They are geo-political and with so many populist leaders, difficult to predict. The Trump tariffs announcement is consistent with his promise to his supporters, but he has yet to implement them, steel and aluminium aside. This may be the way Trump believes he can get China in particular to discuss other trade issues and IP theft. The USA only imports 2.9% of its steel from China. Here are the top 5 exporters of steel to the USA:

1. Canada 16.7%

2. Brazil 13.2%

3. South Korea 9.7%

4. Mexico 9.4%

5. Russia 8.1%

If a trade war was instigated the USA would be the net loser. Take soybean for example. The USA has 42% of the global market for soybean. It accounts for 34% of global production. Half is shipped to China. The next largest producer is Brazil: they would happily supply China if China imposed a 25% tariff on the USA as tit for tat.

The primary U.S. trading partners are China ($636 billion total trade), Canada ($582 billion), and Mexico ($557 billion). The trade deficit with China is $375 billion. It’s responsible for 66% of the total U.S. deficit in goods. The other U.S. trading partners don’t create much of a deficit.

An ongoing trade deficit is caused when a country consumes more than it produces. The United States can buy more than it makes because it can finance the difference by borrowing from its trading partners and encouraging inward investment. The UK is the same.

The solution is never tariffs or trade restrictions. The solution is innovation-led productivity gains with Government help such as tax relief. Since 2015, the tax relief a company can get in the UK has increased to 230% on their qualifying R&D costs.

Loss-making companies can in certain circumstance surrender their losses in return for a payable tax credit.

Encouraging Universities to create strong links with business, particularly in applied research, is another strategy. Good examples in the UK are Loughborough, Nottingham, Cambridge and Aston (Birmingham).

As I write this Trump is moderating his stance, but his threats create uncertainty and this may be one of factors causing the recent softness in the rate of Global growth, apart from the worse than usual weather in March.

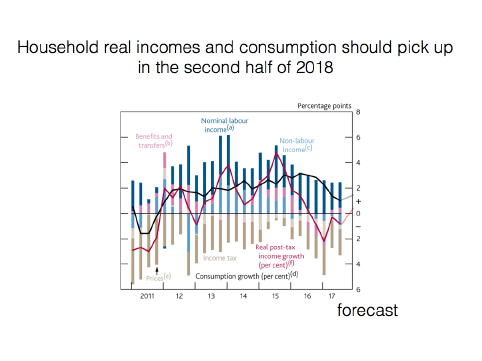

LOOKING AHEAD

UK retail should have an improved second half of the year. Better weather plus real growth in incomes should drive consumption. Regrettably if the price of oil continues to rise discretionary spend will be constrained. Brent is currently $75 per barrel. I would expect it to stay around this level and do not expect $100. US shale supply is very flexible and at

$75 a lot of new capacity is being tapped. However, if we do see $100 a barrel then expect a global slow down.

The EU and the US will continue to grow and together they are driving volumes up for Asian exporters.

The risk is rising global inflation and consequential increases in interest rates.

Here is the forecast for the UK I made earlier this year:

- GDP in real terms will be 1.9%

- Wages will grow at 3.5%

- Inflation will stick at 3%

- Retail sales will improve in the second half of the year

- House prices +1-3% depending on location

- Interest rates 1% by year end

- Exchange rates – so much depends on politics and negotiations

- Given relative interest rates, inflation rates and current exchange rates, Sterling should be weaker against the dollar at $1.33, and 1.12 against the Euro. The chart summarises the possible movements.

Only time will tell!

THIS LAST SECTION IS OPTIONAL READING.

In my discussions with interested individuals there is a common complaint, that the EU is undemocratic, and EU regulations and directives are imposed on us by an unelected body.

This claim mainly refers to the EU Commission, which is the EU’s executive body. It is true that the Commission President and the individual Commissioners are not directly elected by the people of Europe. It is also true that under the provisions of the EU treaty, the Commission has the sole right to propose EU legislation, which, if passed, is then binding on all the EU member states and their citizens.

But the Commission’s power to propose legislation is much weaker than is realised. The Commission can only propose a particular law if EU governments have unanimously agreed to allow it. Thus the Commission can only propose EU laws in areas where the UK Government and the House of Commons has agreed that it can.

Also, ‘proposing’ is not the same as ‘deciding’. A Commission proposal only becomes law if it is approved by both a qualified-majority in the EU Council (unanimity in many sensitive areas) and a simple majority in the European Parliament. In practice this means that after the amendments adopted by the governments and the MEPs, the legislation usually looks very different to what the Commission originally proposed.

In the eighties the Commission was stronger, with less MEP oversight, but the EU has evolved and in the process become more democratic.

Part of the misunderstanding about the power of the Commission is I think because we Brits compare it to our system. The British government commands a majority in the House of Commons, but the Commission does not. And like the current UK Government, the Commission has to build a coalition issue-by-issue. Because of this the Commission is in a much weaker position in the EU system than the British government in the UK system.

The Commission President and the Commissioners are indirectly elected. Under Article 17 of the EU treaty, the Commission President is formally proposed by the European Council (the 28 heads of government of the EU member states), by a qualified-majority vote, and is then approved by a majority vote in the European Parliament. In an effort to inject a bit more democracy into this process, the main European parties propose rival candidates for the Commission President. In 2014 the centre-right European People’s Party (EPP) won the most seats in the new Parliament, and the European Council agreed to propose the EPP’s candidate: Jean-Claude Juncker.

This new way of ‘electing’ the Commission President does not feel very democratic. None of the main British parties are in the EPP (the Conservatives left the EPP in 2009), and so British voters were disenfranchised. There was also very little media coverage in the UK of the campaigns between the various candidates for the Commission President, so few British people understand how the process worked (unlike in some other member states). Thus it is felt by many that the whole thing is undemocratic.

Once the Commission President is chosen, each EU member state nominates a Commissioner, and each Commissioner is then subject to a hearing in one of the committees of the European Parliament (modelled on US Senate hearings of US Presidential nominees to the US cabinet). If a committee issues a ‘negative opinion’ the candidate is usually withdrawn by the government concerned. After the hearings, the team of 28 is then subject to a vote by a simple majority of the MEPs.

Finally, once approved, the Commission as a whole can be removed by a two-thirds ‘censure vote’ in the European Parliament. This has never happened. The last time it happened in the UK was in 1979. But in 1999 the Santer Commission resigned before a censure vote was due to be taken which they were likely to lose. The Commission is not directly elected. But it is not strictly true to say that it is ‘unelected’ or unaccountable.

In so many ways, the way the Commission is chosen is similar to the way the UK government is formed. Neither the British Prime Minister nor the British cabinet are directly elected. Formally, in House of Commons elections, we do not vote on the choice for the Prime Minister, but rather vote for individual MPs from different parties. Then, by convention, the Queen chooses the leader of the largest party in the House of Commons to form a government. To my mind this is like the European Council choosing the candidate of the political group with the most seats in the European Parliament to become the Commission President.

After the Prime Minister is chosen, he or she is free to choose his or her cabinet ministers. There are no hearings of individual ministerial nominees before committees of the House of Commons, and there is no formal vote in the government as a whole. From this perspective, the Commissioners and the Commission are more scrutinised and more accountable than British cabinet ministers. But I find it impossible to convince others who are wedded to a view of the EU as it was in the early days and is not now.

Most EU regulations are safety and performance standards to enable the single market to work effectively and ensure lower quality products do not enter from third countries. EU quality standards are now global. EU regulations are laws voted on and approved by the members of the EU Parliament.

A directive is an agreed objective but it is up to each country to implement it in a way which suits them i.e. by creating local laws by the respective Parliaments. For example we interpret the Working Time Directive quite differently compared to the French.

The House of Commons has sovereignty over all EU Directives. But we have to embody EU regulations into UK law. The unelected House of Lords acts as a reality check on the elected representatives in the House of Commons. The House Lords cannot reject a bill passed by the Commons but they can suggest amendments which may or may not be accepted.

It must be repeated that the UK will not make up for loss of trade with the EU by selling more to the USA (we already have a trade surplus with the USA and Trump will want to reduce that). Nor will trade with the Commonwealth increase sufficiently. So it remains we must ensure trade with the EU is as far as is possible maintained. Current trading arrangements will now remain in place until December 2020. At this stage we do not know what lies beyond although there are all sorts of crazy proposals such as the customs partnership.

This would remove the need for new customs checks at the UK border. The UK would collect tariffs set by the EU customs union on goods coming into the UK on behalf of the EU. If those goods didn’t leave the UK and UK tariffs on them were lower, companies could then claim back the difference. An expensive bureaucratic nightmare.

The other proposal is a ‘highly streamlined’ customs arrangement. This would minimise customs checks rather than getting rid of them altogether, by using new technologies and things like trusted trader schemes, which could allow companies to pay duties in bulk every few months rather than every time their goods cross a border.

My take on this is May playing for time with a divided cabinet. The result will be an extension of the transition period beyond 2020. The EU will welcome this because we will continue to pay our subscription!

Anecdotal evidence suggests that UK businesses with most of their exports going to the EU are increasing their EU presence by creating new capacity within the region. This is a sensible move in case we crash out which is still a possibility.

Rmfagg@aol.com May 7 2018

Roger Martin-Fagg

Roger Martin-Fagg

Roger Martin-Fagg is an economist turned strategist.

A behavioural economist who focuses on behaviour and feedback loops which are largely absent from conventional models.

He began his career in the New Zealand Treasury, then moved into Airline Business Planning and teaching postgraduates all aspects of economics. He designed and ran the postgraduate diploma in Airline Management for British Airways before joining Henley Management College in 1987, where for 21 years he taught senior managers macroeconomics and strategy.

Roger is an independent teaching consultant. He has been external examiner to Bath University, worked with the Bank of England, three of the major UK clearing banks, advised a major London recording studio for 15 years, and regularly talks to SME owners in the UK and Europe about economic trends. He is a visiting fellow to Ashridge, Warwick and Henley business schools.

Roger is a practical researcher. He focuses on how the economy really works and on the links between FT100 reward systems, the behaviour of banks and economic instability. He also researches his clients trading environment as a necessary component of his teaching. His book

“Making Sense of the Economy” is in its fourth reprint.

He speaks at conferences around the world on the economic outlook and its impact on business. His quarterly Economic Update is sent to 1,200 SMEs.

Roger is one of over 70 experts that works with the Property Academy’s members. Want to find out more about the benefits of Property Academy membership and attend a free trial meeting?

Follow our social channels here: