by Roger Martin-Fagg

Currently there is nothing but good news! All the economic indicators are set fair and for the first time in ten years the Bank of England has signposted that interest rate rises are likely within the next two years.

Currently there is nothing but good news! All the economic indicators are set fair and for the first time in ten years the Bank of England has signposted that interest rate rises are likely within the next two years.

For economists it is a perplexing time.

The UK economy is at full employment and yet average earnings are only growing at 2.3%. This is presumably because employers are having to increase pension contributions for employees and keeping wage growth low is the only way to control unit labour cost. I am assuming that the supply of workers from the EU will fall by 700,000 over the next two years partly because of the weak pound but mostly because there is a sense of not being welcome and the EU is growing as fast as the UK.

Historically wages would be growing by 4% given the supply and demand conditions of the current labour market. A recent survey of 1000 employers indicated they average award this year would be just 1%.

If this turns out to be true, then real wages before tax will be falling for many employees and with a time lag so will final demand. The view of the Bank, which I support is that final demand will be maintained as net exports plus investment spending offset the decline in the rate of growth in household consumption.

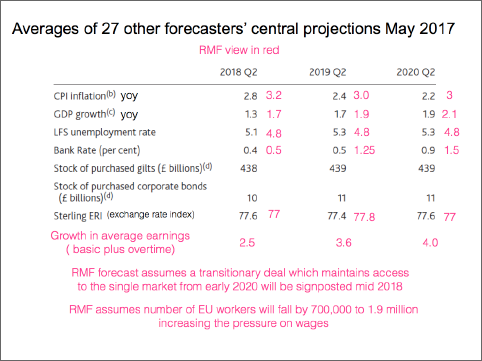

The above chart is the basis on which you should make your own judgement . The key assumption is that the Government gives a clear sign that they and the EU will be able to agree a transitionary deal which in effect will mean business broadly as usual with the EU, from 2019.

I want to take each line in turn. I think the inflation rate will be a bit higher that the average forecast because already retail is absorbing some cost increases in their margin. Owner managed businesses may be able to accept this, but big institutional investor owned companies will not ( the impact on eps and board bonuses will be too severe!) And we are already seeing some companies raising their prices and margins claiming a weak pound as the reason (justified in some but not all cases).

I think the real growth rate will be a bit higher than the average view. This is mainly due to continued expansion in the EU and the USA.

My unemployment rate is lower because there be fewer EU workers available and employers have take what is avaiable. Your next Amazon delivery may even be undertaken by a Brit!

I am bullish on bank rate. Here are the reasons. The Bank are required to assess the tradeoffs between inflation, growth, the level of employment and the exchange rate. Current growth in M4 money is just below 7% yoy. There is loads of money in the UK economy. About 80% of it is financing residential and commercial property new build and keeping up the prices of second hand stock.

The growth in money supply over the past year has enabled the Government to reduce its borrowing by 20Bn.

It has propelled the FT 250 from 17,000 last May to 19,800 today.

Confidence is high because the money supply is boosting investors wealth.

If we ignore weak wage growth, every other indicator is screaming a need for rate increases. And as you can see I expect a 0.25% increase within the next 12 months and then increases to 1.5% by 2020.

Some observers may well suggest that instead of raising interest rates, the Bank should sell some of its bonds and gilts (ie reverse some of the Quantitative easing). But the effect will be the same: long run interest rates will rise as bond and gilt prices fall.

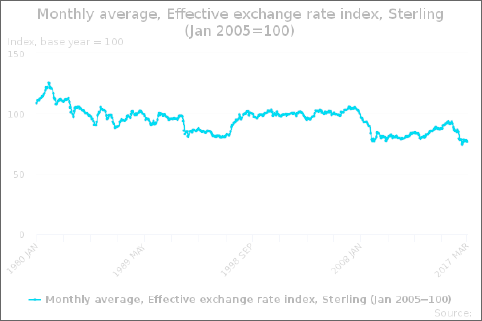

Finally the Exchange rate Index. This is an index of a basket of currencies weighted by the volume of trade we undertake in each currency. Assuming the Government goes for the business as usual, transitionary deal, the index will sit at current levels. This means $ 1.20-1.28 and Euro 1.20 until 2019 when we could see $1.35 and Euro 1.25.

UK house prices

The media have been exercised by the fact that the Halifax index suggest 0.3% fall in house prices in April. The index includes London and prices have fallen in London particularly at the top end. Strip London out, and nationwide prices are stable or rising.

There is a lack of stock coming onto the market, this probably due to the election with sellers waiting to see if there will be changes in stamp duty. The bank of mum and dad is now the ninth largest source of finance for house purchase. However looking ahead, with wage growth slowing, and long interest rates likely to rise, house price growth will fall to around 2% per annum.

What are the implications for business of these forecasts.

75% of the World economy is expanding, in particular the Eurozone. A rising tide lifts all boats, and the UK will be no exception. The next two years will see growth. UK non food retail will see a softening of demand this Autumn and on into 2018 as real wages fall by 1-2%. As the currency hedges have mostly expired, the price in sterling of dollar denominated goods is rising between 10 and 15%. This is, and will continue to put pressure on margins. This cost pressure will be shared between customers ( higher prices) and employees ( limited wage growth).

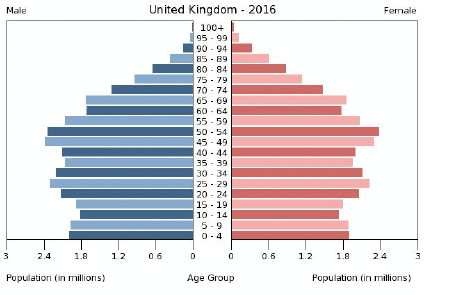

The forecast reduction in the supply of EU labour ( 700,000) will create significant resourcing problems in hospitality, food processing and service, distribution and logistics, health and old age care, labour intensive agriculture, and retail. The response has to be, where ever possible, automation. A look at the population pyramid (next page) shows that those who retire in the next 15 years will be replaced by a smaller number, and they in turn by a smaller number. The increase in the 0-9 year olds will take time to work through.

Money will never be cheaper, so if you have investment plans which require financing, do it now.

The labour market will become even more competitive. Your key staff will be valuable to others. Make sure your business is a great place to work where people feel fairly rewarded but above all recognised, valued, and appreciated. Ideally you should be inundated with calls from people who would like to work in your business!

If you are exporting into the EU supply chain be aware that our neighbours according to a recent survey are planning to do without us. To change their mind we have to be superior in every respect .

More than ever before you must ensure your business is distinctive and compelling. The next 5 years will see significant changes in the way value is added, you must look at your business model and be clear on how and when it must adapt to be fit for purpose. The whole Brexit thing is on top of demographic, societal, and technological change.

The Election

At the time of writing the labour manifesto has just been published. There is a lot there which will appeal to the under 40 year olds with teenage children who are not earning 80k a year. The overall bill of around £75Bn cannot be successfully financed by the top 5% of earners and corporation tax. Denis Healy discovered this fact in the mid seventies.

The proposal to nationalise water supply has merit, particularly if the Welsh Water , not-for -profit model is adopted. Welsh water has continued to invest, it has a long run plan, it doesn’t take short cuts to meet shareholder dividends. In comparison Thames Water Utilities has to grow its earnings per share by 10% per annum. It is owned by the Chinese, Canadians, Saudis, BT pension fund and some Australians. All of whom of course are concerned that investment spending to secure the future is maintained!

And there is merit in renationalising the rail network if only because railways are a public good and will always require taxpayer support. The current set up is a goldmine for lawyers as they handle the continuous disputes between the owner of the infrastructure and the franchise holders. The Swiss railways are generally accepted to be one of the best in the World. 50% of their income is subsidy.

In the UK the franchise holders receive more in subsidy than they return to the Government and 90% of their operating profits are paid out in dividends ( compared to around 65% for FT 100 companies).

The Conservative Manifesto

It is a direct appeal to workers who are disenchanted with Mr Corbyn. The 11 point plan on workers rights could have come straight out of the European Commission! The only problem most of these workers will not know about the plan, whereas their employers will and probably view it with some dismay.

The promise to cap energy prices is flawed. The industry is an oligopoly with 6 major suppliers serving 90% of the market. There will be a game of cat and mouse with the regulator Ofgem. Instead of capping, the Government should legislate for transparency in customer pricing and bills. I like most customers find it almost impossible to work out the best value supplier.

The Libdems

A beefed up British Business Bank owned by the state is a first rate proposal. As is the start up allowance of 2.5K for the first 6 months to entrepreneurs. I like their focus on small business, although offering fathers another month of paid maternity leave will not go down well with SME owners!

The average voter will not have read any of the manifestos. They will be influenced by their choice of media. The one thing that seems to have gained significant traction with the voting public is ‘the bloody difficult woman’ approach to Brexit negotiations. I guess this will give the Conservatives some big wins in marginal constituencies.

The rest of the world

The USA growth rate in Q1 2017 was below expectations mostly due to snow storms. It expanded by 2%. Like the UK, it is at full employment and money supply data shows M3 growing at the same rate as the UK , at just under 7%. The Fed is expected to raise interest rates twice before the year end. So far the big infrastructure spend promised has not materialised and we still await details on tax cuts. The majority of Americans in a recent poll thought the economy would continue to improve but they were less confident their President would!

Europe

Macron is an anglophile but also wishes to drive further integration in Europe. Latest region election results in Germany suggest that Merkel will be re-elected. Poland, Hungary and Romania are moving further to the right.

Meanwhile the EU as a whole is growing at 2%, the same as the USA and the UK.This will continue.

China

There are signs that the growth burst of the past year is faltering as industrial production slowed in April. But as required the announced growth rate was 6.9% ! Electricity consumption figures show a good recovery to around 5% growth rate.

Conclusion

All the indicators suggest stable growth is in prospect for the UK and the World. The UK

will face a severe and growing labour shortage. Interest rates are rising in the USA, and will begin to rise in the UK and the EU next year. Assuming the signs of a soft Brexit come through early on then growth will be maintained. We await the outcome of the election and the negotiations.