by Roger Martin-Fagg

by Roger Martin-Fagg

This month’s update is in two sections.

The first deals with the implications of the latest data. The second is optional reading and discusses what type of Brexit may take place given the political climate.

When will UK austerity end?

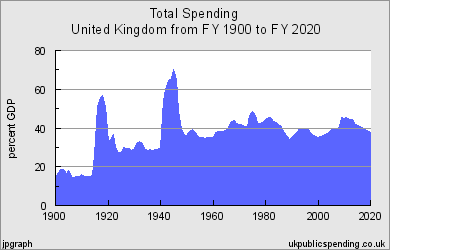

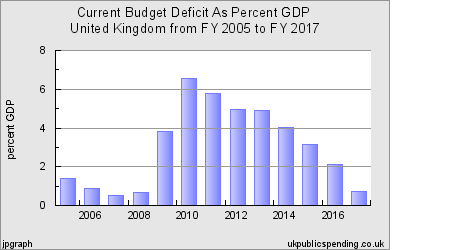

If you look at the chart, since the all-encompassing welfare state was created in 1949, UK public spending has been plus or minus 5% either side of 40% of GDP. In 2017 it will be 40% of GDP. 1% of GDP is £18Bn.

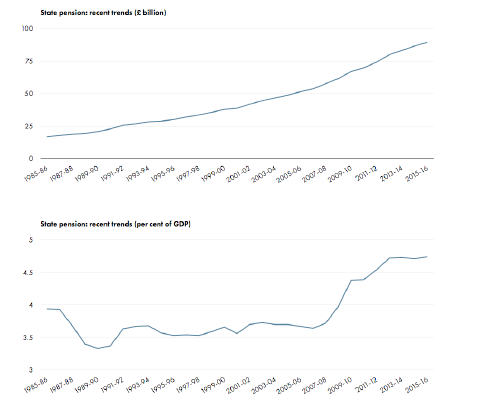

Government cuts across a range of services are the consequence of the triple lock on pensions: this budget has grown by 27% since 2011. It is the single largest component of public spending. As longevity improves so this budget will expand faster than nominal GDP. So, as the government wished to reduce the deficit without raising taxes, other areas of spend had to be cut.

Austerity would be reduced if the triple lock was stopped. The Telegraph would object. So, to survive as leader, May has already dropped the idea.

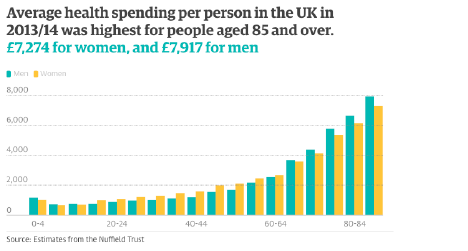

With longevity comes more health spend on the elderly. The average health spend per person in the UK is £2k . But as the chart shows, old people cost 3 or 4 times the average.

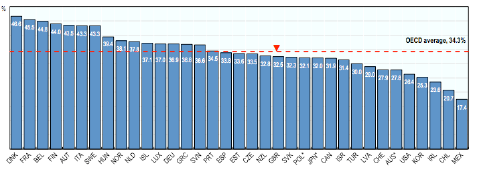

This chart shows government revenue as a percentage of GDP for 2016 from the OECD. The UK (the red arrow) is at 32.5% – below the OECD average.

A lower tax take, plus the desire to reduce the budget deficit which ballooned from 2009 (due to the recession and the RBS/Lloyds bailout) prompted the government to cut areas of spending which people would not notice immediately. The best example is the capital budget, which was halved. This is why there are not enough school places for our growing population.

Recently, I spoke with a senior manager in a global company. His wife, a nurse with 22 years’ experience, applied to be a Ward Sister. The health authority told her there was no budget for the mandatory training. A few weeks later, they employed a qualified Sister from Spain. They also found that their son could not get into their nearest secondary school, and attributed that to the sizeable EU workforce locally, many with children at the same school. They both voted leave. And I would have too in their situation. This is the impact of austerity.

Austerity would end if there was a 2% increase in the tax take. This would raise £11Bn. If the budget deficit were increased by £20Bn we could have £31Bn of new spend. This is roughly what the Labour manifesto proposed.

The data tells us that the UK is a relatively low tax economy, with a small budget deficit (under 1% of GDP) and an ageing population which absorbs an increasing proportion of the national share. Assuming nominal GDP grows at 5% a year from now on, the government can grow its spend by the same amount without raising tax rates or its borrowing.

As I write this there is much comment on the 1% lock on public sector wage awards. Since 2009 the reduction in real incomes for both private sector and public sector employees has been equal at 5%. But the private sector is beginning to forge ahead now, with latest earnings growth at 3.3%. A tight labour market warrants wage awards regardless of which sector. An increase in the rate of tax across the board to pay for higher public sector wages would seem reasonable especially as so many of these workers are looking after the ageing population and hopefully enabling the next generation to be more productive.

1% on the basic rate would be sufficient. There are 5.4m public sector workers and 26.5m private sector workers in the UK.

Currently the amount of money in the economy and its growth rate is quite sufficient to finance higher wage awards for all employees. If the public sector received 2% across the board initially, the budget deficit would increase but after 2 years would be reducing again as new tax revenues flood in. (I am not a leftie but I do understand how the economy works….to some extent!)

However this will not happen given that the Treasury want to have significant borrowing headroom in the event of a hard Brexit recession.

A brief economics lesson for those who think there is no money tree.

The government has no money of its own. Its money is either borrowed from pension funds round the world, or from the central bank (in exceptional cases), or raised from taxes.

BUT

THERE IS A MONEY TREE. It isn’t the Government, it is the UK commercial banking system. Commercial banks create new money out of thin air. Over 80% of this new money is mortgage finance. It is currently growing at 8% per annum and driving up real estate prices. Individuals who own property are benefitting from significant gains in unearned wealth.

It is a fact that perceived unfair taxation of incomes increases the level of avoidance and reduces the income tax yield. The 50% tax rate produced only a third of the expected amount. The principles of taxation demand that it be easy to collect and not act as a disincentive to enterprise and growth.

Taxes should be levied where the most money is. The nation has to openly discuss the taxation of land and property. This is where the money tree’s fruits go. Savills estimate that the growth in property wealth since 2008 is £1.8Tn. The national debt is £1.6Tn. It is easy to see where the ‘money’ is (yes, I am aware it is not liquid).

Where is the UK now?

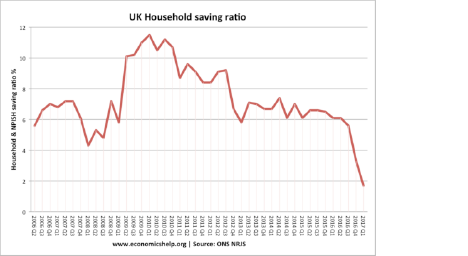

The impact of currency depreciation since the vote to leave has hit households as expected. Real disposable income has fallen 2%. Households have used borrowing and reduced their rate of saving to maintain their spending.

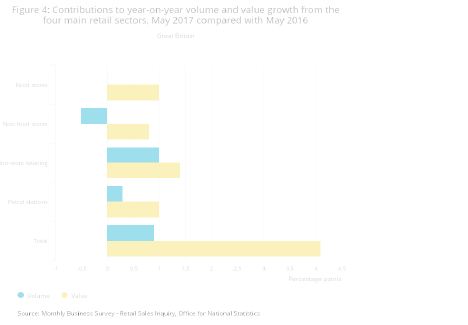

The chart shows that over the past year the value of retail sales has grown by over 4% but the volume by just over 0.8%. The reduction in real incomes is beginning to bite.

The latest data on private sector earnings is a glimmer of hope. Before tax earnings are growing at 3.3%. This is roughly in line with inflation and if it continues will give a small volume boost to retail sales in the autumn.

The latest PMI index shows a small but not insignificant reduction in confidence: the forecast was 56.5, the actual 54.3. The index is notoriously volatile but has been on a downward trend since May (I was pretty optimistic then, but the election has changed sentiment and the outlook is bleaker).

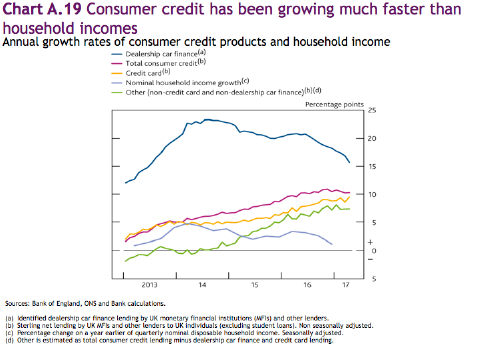

The latest financial stability report from the B of E shows the Bank is now worried about the quality of some bank lending particularly for car purchase, some mortgages, and unsecured lending (this excludes student loans which are underwritten by the taxpayer). It is asking banks to increase their capital buffer by 1% and is bringing forward its stress test of the system to the early autumn.

MPC are steadily moving towards a vote in favour of an increase in interest rates by the end of October.

House Prices

Assuming mortgage availability and mortgage interest rates are unchanged, the remaining driver of house prices is real incomes plus whatever is written in the Mail and Telegraph.

Real income growth in 2016 supported house price growth of 6% year on year this April. Real income growth today suggests house price growth of zero to 1%. I do not expect a price crash. For those of you who are sellers at the top end of the market (£2 million plus) you will need to take a sizeable hit if you want a sale (unless you took the advice of your agent and priced it correctly). For mere mortals below £900k, the market will not collapse but we should expect low or no increases until 2019. A hard Brexit with no transitional arrangement could cause a price crash after March 2019 due to a collapse in confidence.

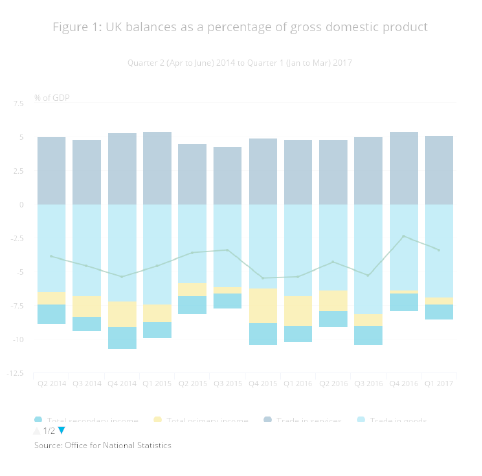

The Balance of Payments

Despite a strong upturn in the EU economy, and a 16% devaluation, our current account deficit has increased. Export value of goods and services has fallen and the value of imports has risen. In fairness this is the accounting impact of a devaluation.

The accounts are written up in sterling so a devaluation makes imports larger by value and exports smaller by value. There are those who believe that over 18 months volumes respond. That is that the volume of exports increases and the volume of imports decreases. I accept that imports will reduce (because real incomes are falling) but I doubt if export volumes will pick up significantly. Most of our exports are sophisticated, price insensitive, high technology goods. Those people around the world who want this type of product are already buying them regardless of trade deals etc. Export volumes are increasing with the EU (up 2.5%) but falling with the rest of the world as a result of the latest revisions to the data.

The good news is we are able to finance our deficit at current interest and exchange rate values. Long may this continue with the generosity of foreigners.

The NIESR has modelled the impact of hard Brexit. We lose 22% of our exports (to the EU) and gain 5% to the rest of the World. This implies a significant continuing current account deficit.

Unless there is a wage explosion, or the inflation rate drops, or there is a surge in exports, or a surge in investment, the data so far suggests the economy will slow sharply over the next 18 months. This is a significant change since May when the data looked encouraging.

The change has been caused by the election.

The latest Deloitte Survey shows 72% of CFOs expect some negative long-term effects on the business environment as a result of the UK’s departure from the EU.

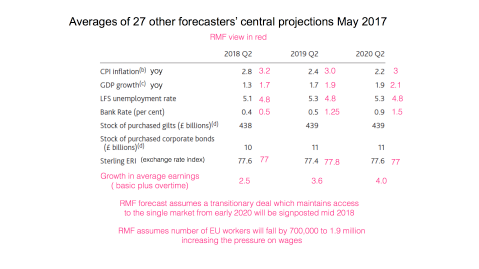

I reproduce below my May forecast.

The impact of the election result on confidence suggests to me that my forecast could be the wrong side of optimistic (i.e. plainly wrong). But we need to wait until October to be sure.

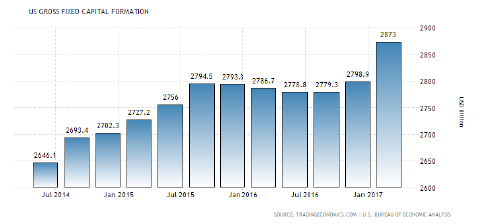

The USA

The first observation is that the Americans knew what they were doing when they set up their system of checks and balances on Presidential power. President Trump has not achieved much in policy terms but I still believe his style and approach continues to give US business confidence and from this flows new investment and growth. Investment spending is growing

strongly.

Retail sales growth is holding up well: sales have not fallen as reported in the media, the rate of growth has slowed!

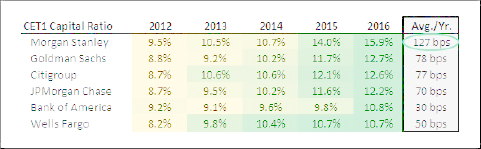

The US banking system is now well capitalised and able to withstand a significant hit from bad debts. A deep recession is highly unlikely. The chart shows shareholders’ funds as a % of the balance sheet. This is mostly retained profits.

It is true that as US interest rates rise there will be an increase in defaults, but although tough for the individual it will not break the system as in 2008. And rates are rising because the US is at full employment. Growth from now on will require greater capital investment which seems to be happening.

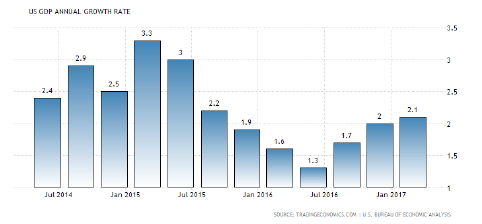

It is surprising that wage growth is still subdued. Only employers will know why. But real wages are still rising at around 1.5% per annum. I expect US GDP growth to continue at around 2.3% per annum with the increase in capital spend boosting labour productivity and real wages. I do not expect a US recession. However if Trump is impeached then things could deteriorate quickly.

The EU

For the past 18 months I have argued that the EU GDP would respond to the massive monetary stimulus from the ECB and it is doing so.

The political climate has changed. President Macron will boost French confidence, investment and growth, the Dutch have remained in the middle ground, Merkel will probably be re-elected.

The Euro area PMI index is at record highs (the UK is at 54)

It is clear that the EU will enjoy a period of stable growth, led by Germany but with strong recoveries in Spain, Portugal and Ireland. As this happens, the budget deficits of member states will fall significantly and there is likely to be a renewed sense of purpose in the European Commission. Capital spending is strong.

Conclusion

The USA and the EU and the UK are all growing at around 2%. The USA at 2.1% is below its trend growth but has reached its capacity ceiling. The EU is growing slightly faster than long run trend. This suggests interest rates should rise in both regions. The UK is suffering from the impact of devaluation, underinvestment by government and large companies, a loss of confidence, falling real wages, the likely loss of skilled EU workers, and the prospect of losing frictionless access to the largest and richest market on earth. It also needs an increase in interest rates to curb credit growth. It will be the first increase in ten years with unpredictable consequences. All this is likely to reduce real GDP growth over the next 12 months to around 1.7%.

I am conscious that this update is in so many ways less optimistic than my last one. I am reflecting data we have to date. I wish it were different.

If you are clear on what it is that makes your business distinctive and compelling then regardless of overall economic conditions you will thrive and in the event of a sharp slow down or even a recession survive. You should only worry about the things you can fix.

Snapshot for next 12 months, UK.

Base rate increase to 0.5% In October

Inflation well above forecast at 3.8% in November.

Merkel victory sends £ to 1.09 Euro

£ stable at $1.28

Net migration falls by 170,00 in 2017

July Economic Update section 2

This section is relevant to those who are trying to make sense of the current political scene

and its implications for Brexit.

When forecasting up to two or three years ahead, normally one can take the Governments’ vision and objectives and work through the implications for consumers and businesses and their economic prospects.

As I write this there is no clarity from the Government, so I will begin with my assessment of where I think things currently stand and then make some forecasts based on this which will be in section 1. I do not claim to be right. I am a patriot but not a nationalist, and I am fully aware of confirmation bias which is humans only select information which supports their point of view.

The first May Government was committed to hard Brexit based on a narrow majority for leaving the EU. This means putting sovereignty first (getting our country back from the unelected suits in Brussels) at the expense of close economic ties.

The European Court of Justice (ECJ), the free movement of EU workers, the customs union and the single market would play no part in British life.

The election changed this. May is substantially weakened, the new Parliament is unlikely to pass all the legislation required for a hard Brexit even with the support of the DUP.

There is now likely to be a softer Brexit but what it might it look like?

The Queen’s speech contained eight key items of legislation which Parliament will vote on over the next two years.

The repeal bill will transform all 19,000 pieces of EU rules and regulations into British law. And then Parliament must legislate on immigration, fisheries, customs, nuclear safety, international sanctions,trade arrangements,and agriculture.

The negotiation with the EU now underway is about the divorce agreement. Only when this is agreed can we negotiate the future relationship.

The labour party won 40% of the vote (the Tories 42.3%).But such is our democracy, the Tories have 317 seats and Labour 262 seats.

Many voices are is calling for a softer Brexit believing this to be the new will of the people (this is difficult to prove).

Ruth Davidson the leader to the Scottish Tories has called for a softer Brexit. Michael Gove the once hard leaver has joined the cabinet and is suggesting a rethink.The DUP who hold the balance of power in Westminster want to keep the open border with the South.

The cabinet and the country are divided.

May lacks the authority to impose discipline within the cabinet. Boris Johnston is as usual an unguided missile with no grasp of the details and pro cake and eating it. Hammond wants more cake for everybody. Liam Fox wants to leave the customs union so he can do trade deals with the rest of the World.

Many voters see both Boris Johnston and Jeremy Corbyn as authentic.

In so many ways Corbyn and Johnston are similar. They are both prisoners of the past, and neither has any grasp of economics. Johnston wants to know ‘what this customs union thingy is’ . Corbyn thinks companies and the top 5% of income earners will fund his economic programme.

The facts are these: 25% of income tax receipts are paid by 0.5% of UK adults, and 50% is paid by 3% of UK adults. 1% on income tax raises £5.5Bn, 1% on NIC raises £4.9Bn, and 1% on Vat raises £5.2Bn.

Unfortunately the electorate is for the most part ill informed. Some believe there is a Government money tree, others believe the EU is an unelected behemoth which for 40 years has crushed British dynamism and its ability to sell world class products and services around the World. They appear to be unaware of the success small and medium sized German companies are having exporting round the World from the EU. Last year Germany exported $80Bn to China. The UK $15Bn.

Sun readers have an average reading age of 8. The Guardian of 14. The 400,000 FT readers are mostly London based with an average reading age of 14. The Telegraph has a million readers, their average age is 61, reading age unknown but they are always wondering where they they left their glasses and why they walked into the room!

Many eurosceptic MPs are backing May in the hope she will deliver a hard Brexit. They have threatened her with a leadership contest if she wavers. The Mail and Telegraph support their views.

May has to have two scripts: one for the hardliners and one for the rest. And this makes it impossible for her to lead effectively.

It is a mess but what will be the likely outcome?

I am assuming a transitional deal, followed by a new customs union with the EU. A customs union is a trade bloc which creates a free trade area behind an external tariff. Within the trade bloc there are no customs duties so goods can move freely between member countries. The customs union negotiates with other blocs and countries for mutually beneficial tariff reductions. After 4 years of negotiations the EU is about to sign an agreement with Japan. The EU and Japan together account for 20% of Global GDP and 39% of exports.

A softer Brexit is a combination of four things.

First some limited curbs on the free movement of labour. This already happens in the EU. Belgium deports EU citizens who do not work and cannot support themselves, Germany is limiting EU workers in their construction industry to keep wages rates up. When workers from eastern Europe flooded into the UK in 2004 it was not Brussels who demanded it, it was the Blair Government. Brussels points out that the UK is much more lax than other member countries in checking residency, giving unqualified access to health care, and welfare benefits.

The first thing we should do is tighten up our procedures.Then agree some sort of emergency brake which the UK could apply if required. However the net flow of EU workers will fall steadily over the next 5 years due to greater opportunities in an ever growing EU.

Second the UK will stay in the EU regulatory agencies. There are 34 key agencies which affect food, air travel,drugs, the trading of bonds and shares to name a few. These agencies play a crucial role in ensuring common standards across the customs union. It would make no sense for us to duplicate them, especially when funds are limited.

Third the ECJ would continue to oversee and rule on trade and regulatory matters. This would be necessary to ensure the customs union worked without friction.

Fourth the UK would agree a customs union with the EU, within their existing customs union.

So for the electorate we leave the existing customs union, but join a new one in out own interest and on our terms.

It is this which is crucial for the prosperity of the UK. The new customs union would mean Britain accepts the common external tariff, enjoys free movement of goods without new paperwork across the 26 countries, and existing supply chains would not need to be reconfigured.

Liam Fox would protest because the UK would not be allowed to negotiate free trade agreements in addition to the 56 countries already agreed for us by the EU. These agreements only cover goods and agriculture. Fox is at liberty to negotiate services free trade agreements with whomsoever he wishes. These are notoriously difficult which is why there are few in place round the World.

The timing. We leave on March 29 2019, immediately we agree a transitional deal which will look like the above. This deal then becomes the new arrangement: we are not in the EU but we are agreeing to a customs union to protect jobs and maintain growth.

If the hard brexiteers in Parliament reject this, then the next PM in 2022 will be Jeremy Corbyn. It’s their call.

Follow our social channels here: