by Roger Martin-Fagg

It is often said there are two types of forecasts…lucky or wrong!

Institute of Operations Management

There are two main types of forecasters: Hedgehogs and Foxes. Hedgehogs know one big thing; they have an all encompassing world view and look for facts which confirm what they already know to be true. Foxes know many little things, they are eclectic in their data sources and nuanced in their judgements. Hedgehogs command more attention but foxes make better forecasters.

There are two main types of forecasters: Hedgehogs and Foxes. Hedgehogs know one big thing; they have an all encompassing world view and look for facts which confirm what they already know to be true. Foxes know many little things, they are eclectic in their data sources and nuanced in their judgements. Hedgehogs command more attention but foxes make better forecasters.

We humans long for certainties but we know we cannot have them. I will make some guesses for 2016 and show you how lucky or wrong I was for 2015. I am a hedgehog.

I have copied and pasted the italic piece below from my February 2015 update.

Forecasts made in Jan 2015

There will be no increase in interest rates in 2015 CORRECT .

I forecast 2.7% UK GDP for 2015

WRONG :LATEST REVISIONS SUGGEST IT WILL BE 2.3% BUT I EXPECT FURTHER UPWARD REVISIONS WHEN THE ONS HAVE SORTED OUT THE CONSTRUCTION SECTOR DATA.

I forecast OIL at $35-$40 for 2015. WRONG: AVERAGE $46 for 2015

I forecast £-$ in the range of $1.50-$1.60, CORRECT. AVERAGE $1.52

I forecast £1 = €1.26 but with volatility. WRONG AVERAGE €1.33 .

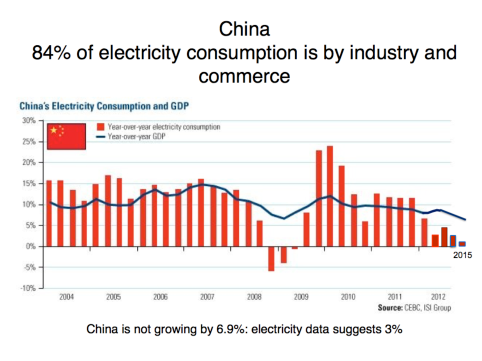

I forecast a sharp Chinese slow down. CORRECT. CHINA OFFICIAL FIGURE OF 6.8% IS A LIE. USING ELECTRICITY CONSUMPTION DATA 3% MUCH MORE LIKELY.

I forecast strong USA recovery, it will strengthen to 3.4% . WRONG: LIKELY TO BE 2.4%

I forecast 1% GDP growth for the Eurozone. THIS WILL PROVE TO BE CORRECT WHEN ALL THE DATA IS IN.

I forecast UK inflation at 1.8%. WRONG: GOODS AND SERVICES +0.85% FUEL AND FOOD -0.8% OVERALL CPI +0.2%

I forecast UK average house prices at 3-5% WRONG : ACTUAL 5.2%

A look around the World

The Conservative party will win an outright majority of between 4 and 10 seats in the UK

WRONG IT WAS 12 SEATS

The hottest growth region will be ASEAN countries averaging 6% CORRECT

The Middle East will slow sharply as a consequence of social unrest, low oil prices, and war CORRECT

Brazil will struggle. Its offshore promised oil bonanza now in question. CORRECT GDP -3%

Venezuela will implode. CORRECT

Russia will shrink 5% WRONG GDP -3%

China will continue to slow down, settling at around 4-5% GDP and punch its weight in the South China Sea CORRECT

India should see a surge in growth to 6-7% CORRECT

Australia much slower growth, a weakening dollar, but she’ll still be right mate! CORRECT

Mexico will grow around 1.7%, the fall in the price of oil is the main depressant. WRONG GDP +2.3%

Companies who borrowed cheap USA Dollars are faced with a significant increase in financing cost as the US Dollar rises against the basket of world currencies. The IMF say 1.8 trillion dollar loans are affected. There will be significant weakness in the Indonesian Ringit, the SA Rand, the Argentine peso, the Brazilian real. CORRECT

The collapse in commodity prices is hurting companies in the value chain, and the banks who have lent to them CORRECT

Overall Conclusion

The US and UK banking systems are now fixed. The EU system will mend more quickly with QE but it will take a couple of years.

Oil importing countries will grow faster than the big macro models forecast, oil exporting countries will contract by more. Notice that for China and the USA the effect is broadly neutral. WRONG ON OIL IMPORTING CORRECT ON OIL EXPORTING COUNTRIES.

Headmasters Report

It has been a patchy performance: welcome progress in some areas but underperforming in others.

The following is a quote from my 1961 grammar school report: for most pupils there is a strong correlation between ability in music and maths. Martin-Fagg has proved to be an exception.

I scored 100% in music and 7% in algebra. Both subjects were taught an inspirational music teacher who unable to teach us algebra! He was unable to answer any sensible question such as what is the point of algebra and who invented it. Like so many 12 year olds I switched off completely.

Now for 2016 forecasts

The UK

Although earnings growth slowed in November I expect earnings ( ie wage growth plus overtime and bonuses) to be between 3% and 4%. This is because there are now 2 vacancies for every unemployed person. Employers will want to keep good staff and raise salaries to do so.

Please note that if CPI inflation stays below 1%, then earnings growth at 2.5% or more will increase real wages at least in line with long run trend.

I expect CPI inflation to be +1.5% by the end of the year ( domestically produced goods and services rising by +2.5%, but Chinese origin goods falling by 5% due to a further devaluation of the Rnb.

The reason is straightforward: with the higher minimum wage, labour shortages, and auto enrollment pension contributions, labour costs will be increasing at around 6%-9% depending on the sector. It is doubtful efficiency can be increased enough to compensate. So prices will be raised.

I expect real GDP to be +2.2%. However if there is an early referendum in July with a vote to stay in, then I expect 2.6% as post vote investment spending will pick up again.

I expect nominal spending to grow by +3.7%; within this consumer spending will be +4.5%, investment spending will slow sharply by big corporates because FD’s, after an unusual surge in optimism, are now reverting to type and have become more cautious.

The external trading account ( the balance of payments) will be continue to be a drain in our flow of spending. And the uncertainty over Brexit weighs on funding and investment choices.

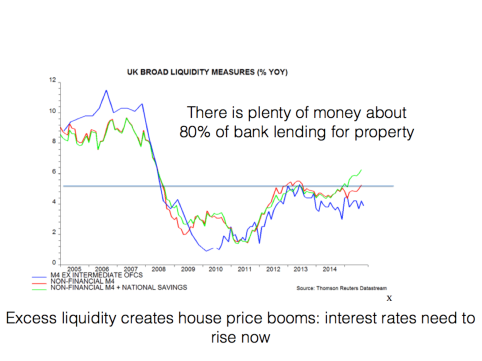

I expect base rate to rise in April by 0.25% and again in October by 0.25%. The reason is this. Assuming the velocity of money is reasonably stable( ie consumer confidence doesn’t collapse) then the rate of growth in liquidity today will drive nominal GDP within 9 months, and price increases within two years. I expect the Bank of England to argue in April that they are increasing base rate because liquidity growth( ie money held in current and deposit accounts plus national savings) will drive spending. The will also state that the weakness of sterling particularly against the dollar represents monetary loosening, and that an increase of 0.25% will strengthen sterling sufficiently to offset this. And as the economy moves towards full capacity prices will increase. The chart below shows liquidity growing at 6.2% in August last year. We await new data due in February.

Sterling will be $1.40 up until March, then $1.48 before reaching $1.50 by year end.

Sterling will be €1.30 up until March then €1.36 before reaching €1.38 by year end. ( assuming ECB continues its programme of QE)

Please note the above assumes the Government is able to show the nation that the future of the UK is best served within a reformed EU. If it fails in this and there is a media frenzy for Brexit, we should expect a sterling crisis. Generally I do not think it sensible to buy currency forward. However as this year progresses if you have currency exposure then it would be prudent to fix if it looks like the nation might vote to leave.

House prices; Nationwide average +5%, London sub £3 million +7%, but top end speculative property prices I expect to fall by another 10%, the bubble has been pricked by changed expectations from Russia, China and Hong Kong.

Government revenues should rise by £30Bn and its spending by £20Bn, thus the deficit will fall by £10Bn but the Government will still be spending 50Bn more than it is earning. This is still an expansionary fiscal stance, in no way can it be described as austere.

The press is full scare stories concerning the growth in credit: personal debt in growing at 8% per annum. 2.63million new cars were sold in 2015. Ford say that 94% of all sales were bought using Personal Finance Contracts. Credit is money, it drives activity.

Europe

Apart from Greece all Eurozone members are now growing again. Spain and Ireland are doing really well, France is not. The whole migration issue has clouded the fundamentals which have improved. The Brussels based European Systemic Risk Board is operational with a remit to limit systemic contagion if a bank fails. It requires banks to hold more capital if their loan book is viewed as risky. It is of interest that at present Norway and Sweden are the only countries with banks required to hold an extra 1% under the new rules. The UK has it’s own rules which are tougher.

There is a tendency to forget that the EU is the biggest, richest single market on the planet. Per capita nominal GDP is $35,000 ( China is $ 7,500 and the USA is $52,000)

Because it is rich and aging its growth rate will never be above 2.5%, but it will consume the broadest range of goods and services.

The ECB continues to create new money by purchasing bonds from the market which has reduced bond yields to below zero for countries like Germany. And the Euro has weakened particularly against the US dollar. A weakening currency automatically boosts the margins of exporters which will boost share prices. It is all part of the monetary expansion feedback loop designed to raise the inflation rate vis growing confidence, spending and output.

It is clearly working.

Stockmarkets

Over the past six years monetary expansion through quantitative easing in the USA, UK, EU and China has driven share prices above earnings growth ( the evidence is higher than long run average P/E multiples). Apart from China and the EU, no further QE is expected. Thus share prices will either stabilise and wait for profits to rise to justify the price or will fall to match the current level of profits. Given the return on bonds is so low it is likely that share prices will pause rather than crash. The FT 100 is down 5% for the year 2015, but this is almost all due to oil and mining stocks which have crashed.

So far this year we have seen China’s failing economy and stock market crash infecting other stock markets. This is absurd. The Chinese stock market does not reflect the realities of China’s economy, it is merely a casino driven by credit availability. We can expect it to be volatile and on average significantly overpriced.

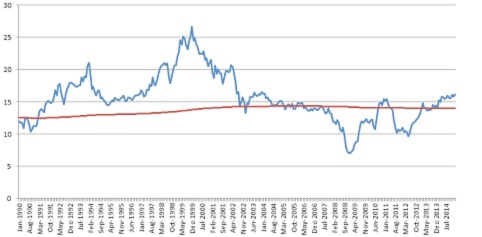

The FT 100 P/E since 1990 compared to the average P/E

The Footsie is on a P/E of 16.7 compared to 15 long run average this implies an overvaluation of 7%. But if we take the cyclically adjusted P/E which averages company profits over 10 years ( the cycle is typically 7 years) it has averaged 20.8 since 1983. Today it is 14.9. This suggests the market is undervalued!

As 80% of Footsie profits are earned in dollars, a further weakening of sterling against the dollar will boost reported earnings and is another reason to suggest that rather than fall further, it will stabilise around 6000. The yield is 3.4% which is better than most if not all cash deposits.

Please note that the most frequently traded shares are traded by machines which are pre-programmed. This always causes a decline in price to gather momentum until a floor is reached, at which point the machine issues buy instructions and the momentum is upwards. The major stocks are not moving based on human assessment of risks and realities. All the algorithms will be out of date, based on assumed, historic drivers of share prices. Hold tight, the markets will recover as quickly as they crash.

The major stockmarkets have been valued beyond fair value for years. And it is reasonable to expect low or no growth from levels established in the middle of last year, that is until corporate earnings rise to catch up with the valuation. Personally my SIPP is mostly equities and I am sitting tight.

China

My regular readers will know that I have been bearish on China for quite a long time. The evidence is now clear, China is finding it difficult to transition from a capital investment led growth economy to a services based system where human capital rather than physical capital creates the added value we call economic growth. Every country in history has found this transition difficult, we should not be surprised.

However the Chinese authorities are going inflict pain on the rest of the world as they try to mitigate the impact on themselves. They will probably devalue their currency by 10-15%, they will allow state owned enterprises to sell at prices close to marginal cost, they will prop up failing financial institutions, and they will get VERY upset when the west begins to raise tariffs to protect domestic producers from dumping.

This is a major risk to the global economy. I would have expected the EU to react more quickly by raising tariffs. And I would have expected it to be a keynote session at Davos this week.

An angry and upset China could do some stupid things in the South China Sea this year.

These are known, unknowns!

The Rest of the World

The rebalancing of the global economy continues in favour of the more mature economies, this trend has been underway for nearly 5 years and it is continuing. Overall I expect the world GDP to grow at 3%. The pessimists think the Chinese slowdown, plus falling commodity and oil prices will cause the global system to struggle. Spending power in the global system is shifting back to the ‘old’ mature economies. This will be sufficient to keep global growth going. I do not understand the establishment view that falling oil prices are bad for global growth. Yes there will be real problems for Aberdeen, Russia, Saudi Arabia, Nigeria, and the banks over exposed to US frackers. But there are much bigger opportunities as cheap oil boosts real incomes. Spending power is shifting from oil producing countries who tend to save in huge sovereign wealth funds, to countries who are living beyond their means as indicated by the size of their Government deficit and usually their balance of payments deficit. The UK is such a country. Low oil prices are on balance a sizeable stimulus via increasing real incomes.

The low or no growth economies are Brazil (-3%)Russia (-3%), South Africa 0.3%, China +3% Saudi Arabia

The growth stories will be the USA (2.5%), Japan (2%), Europe (2% including the UK), India 7%, Mexico 2.5% , Indonesia 5%

The oil price will stay below $40 unless there is an unforeseen collapse in supply from the middle east due to Sunni vv Sharia vv Isis or some other peculiar unknown!

Some commentators are using the oil price as evidence of a sharp drop in demand due to faltering growth. They are wrong. Oil consumption in the USA rose 6% in 2015. The price drop is due to excess supply which is in turn due to Saudi Arabia determined to keep its market share. Eventually the Saudis will see their plan is a mistake, but I guess it will take time. Meanwhile enjoy $30 a barrel!

The biggest risk to the UK this year.

The biggest risk is the run up to the referendum on EU membership and a possible exit.

In my judgement this is top of the risk to growth list. It has the potential to cause a recession and then a lower rate of growth thereafter.

In brief.

The UK runs a trading account deficit with the rest of the world. This has to be financed. It can be financed by stable long run capital investment in the UK from international companies, ( something we have enjoyed since the early eighties because we are inside the EU external tariff wall). Or by spending our reserves of foreign currency ( we have about 6 months supply). Or by attracting short term financing ( requires higher interest rates). Or by devaluation. Or a combination of the above.

If we lose long term investment inflows to other EU members then we have to resort to short term financing and interest rates have to be used to keep the flow up. This would be a disaster for growth. Imagine interest rates rising to 5% in 2017.

On the street, people believe that if we leave we can control our borders. This is only true if we no longer wish to sell to the largest market in the world ( currently 15% of our GDP is derived from selling to the EU).

If we want to have access to the EU markets, we have to abide by the 4 freedoms, one of which is the free movement of labour.

Norway is not a member of the EU but it has access to EU markets. It has 7.38 EU migrants per 1000 population.

Switzerland is not a member of the EU but is also has access to EU markets. It has 11.33 EU migrants per 1000 population.

The UK is a member of the EU it has only 2.48 EU migrants per 1000.

These facts will never be written in the Mail and probably not in the Mirror and Sun. Their combined readership ( paper and online is 33.5 million).

If we vote to leave.

Firstly we would have to adapt most of our legislation to remove the EU directives. EU treaties with the rest of the world would cease to apply to the UK. This would take up to 10 years.

Secondly we would need to negotiate with the EU on the future of the 2 million Brits who live there.

Thirdly under WTO rules we would have no right of access to EU markets our goods and services would be subject to tariffs. We would have to make significant payments as do Norway and Switzerland to gain access.

Fourthly we would have develop trade with the rest of the World. Current EU trade deals cover 60 countries and 35% of world trade. These would no longer apply to us, we would have to start from scratch and we would be up against the EU’s much bigger bargaining power. It could take 20 years.

Given how long it takes to agree trade deals on a bilateral basis, I would guess we would have years of economic misery before the deals were in place to allow us to trade.

Over the next six months, if the UK press and media report that an exit is a growing likelihood, then we must expect a sterling crisis.

This would take sterling to $1.20 or below and € 1.10 or less. I do not usually recommend buying currency forward, but if you are exposed, do it now.

Rmfagg@aol.com 21 Jan 2016

Roger Martin-Fagg

Roger Martin-Fagg is an economist turned strategist.

A behavioural economist who focuses on behaviour and feedback loops which are largely absent from conventional models.

He began his career in the New Zealand Treasury, then moved into Airline Business Planning and teaching postgraduates all aspects of economics. He designed and ran the postgraduate diploma in Airline Management for British Airways before joining Henley Management College in 1987, where for 21 years he taught senior managers macroeconomics and strategy.

Roger is an independent teaching consultant. He has been external examiner to Bath University, worked with the Bank of England, three of the major UK clearing banks, advised a major London recording studio for 15 years, and regularly talks to SME owners in the UK and Europe about economic trends. He is a visiting fellow to Ashridge, Warwick and Henley business schools.

Roger is a practical researcher. He focuses on how the economy really works and on the links between FT100 reward systems, the behaviour of banks and economic instability. He also researches his clients trading environment as a necessary component of his teaching. His book

“Making Sense of the Economy” is in its fourth reprint.

He speaks at conferences around the world on the economic outlook and its impact on business. His quarterly Economic Update is sent to 1,200 SMEs.

Follow our social channels here: