The latest economic update from one of the best economic forecasters in the UK, Roger Martin Fagg.

The latest economic update from one of the best economic forecasters in the UK, Roger Martin Fagg.

Many of Property Academy’s Members have had the experience of working directly with Roger in our mastermind group meetings and all our members receive his regular economic briefings.

Roger called the last shock General Election result and accurately predicted that Trump would be President months before anyone else. You can find more information about Roger, the many other benefits of Property Academy membership and apply to attend a Mastermind Group session at the bottom of this update.

In addition to his usual summary of world events, in this update, Roger writes a very honest personal ‘school report’ – comparing his recent predictions against actual performance. He may not always be right, but in the words of famous British Economist John Maynard Keynes, “It’s better to be roughly right than precisely wrong” and Roger is certainly top of his class.

It is an iron rule of history that what looks inevitable in hindsight was far from obvious at the time. Today is no different. Will China continue to move up the value chain and overtake the USA by 2035? Will the EU reform its institutional arrangements following Brexit and the EU elections in May? Will the oil price hit $85 at the end of 2019, pushing the global system into a significant downturn? Will higher US interest rates magnify the effect? What will Trump do next?

In ten years, historians will look back at 2019 and write that the answers to all these questions were obvious.

There are two kinds of chaos. First level chaos is chaos which does not react to predictions about it. The weather exhibits first level chaos. The weather forecaster has no impact on it. More data, supercomputers and better graphics produce higher quality and more accurate forecasts. An aged Welsh hill farmer is usually accurate in her short-term forecast because she has experienced so much weather in her lifetime.

Then there is second level chaos. Level two chaos reacts to the predictions made about it. The economy and politics both exhibit level two chaos. In both cases, a small change is magnified by the systemic response. There is always a positive feedback loop at work. Both these effects can be seen today; and the two systems are inextricably linked.

This makes accurate forecasting impossible. If a forecaster gets it right, it is down to luck, not a superior model or brain.

We humans use forecasts to either confirm or deny our judgements. We are all subject to confirmation bias. This means we will accept and value any forecast which supports our point of view. And disregard any forecast which suggests we are wrong.

I see myself as that Welsh shepherd: I have experienced lots of economic weather, but regrettably, this time around, the political variables are complex, unusual, and ever changing. All I can do is to look at the broad economic indicators and express an opinion on how the political scene will impact on them.

In my previous update I looked at the key forward indicators. I will update you with the latest.

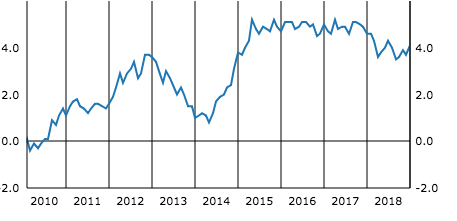

Indicator 1: The money supply and bank lending.

The money supply is the oil which lubricates the economic engine. We measure economic activity in money terms. We assess our wealth in money terms. The nominal GDP of the UK is £2.2 trillion. The wealth of the UK is estimated to be around £10 trillion.

For nominal incomes to grow at around 4% per annum, money supply has to grow at around 5% per annum. There are losses in our system due to money lying idle or changing hands more slowly which is why we need 5% growth to produce 4% nominal GDP.

The graph shows a significant reduction in the rate of growth in money supply, which if sustained, will ensure lower real growth at the end of this year, and into next.

As a consequence, it is unlikely that interest rates will rise this year. It is conceivable the Bank of England will implement more QE if money supply remains at 2% or less growth.

The chart shows that bank lending is growing at 3.2%. Anecdotal evidence suggests that some of this growth is to finance stock building ahead of possible supply chain disruption after March 29. The bulk of new lending is for real estate which is why house prices were growing at nearly 3% at the end of last year.

Unusually, money growth is less than lending growth. This is probably because large multi-nationals are choosing to hold euros and/or dollars instead of sterling. Again, the result of political uncertainty.

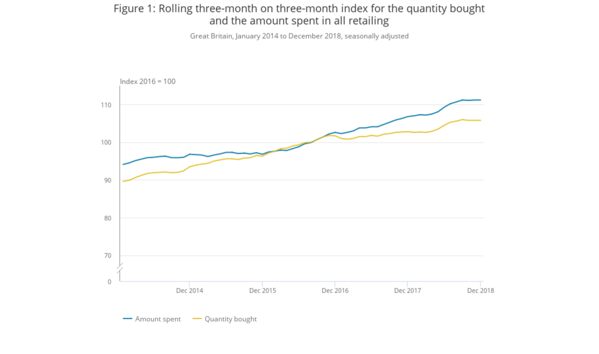

Indicator 2: Retail spending

Retail spending, both online and on the high street, accounts for 22% of nominal GDP. It is a good indicator of money supply flow through our system. The chart shows that since the middle of last year, spending has been flat, both in money and volume terms. Most retailers would agree.

The question for 2019 is – will retail spend return to growth?

Latest data for November shows nominal wages growing by 3.2%; the CPI index including housing costs grew by 2%; real wages before tax growing by 1.2%. It is unlikely that employers will, on average, raise earnings above 3.2%, due to Brexit uncertainty. And inflation this year will depend primarily on energy costs (a 33% weighting in the CPI index), which in turn will depend on oil prices and the sterling dollar rate.,

As the global economy begins to slow, oil prices are likely to remain at current levels as the Saudis cut back production in line with slower growth in demand from Asia. Brent Crude is likely to remain at $62 this year.

The value of Sterling is crucial. A 10% fall flows through to a 2% increase in CPI, according to the Economist. And the value of Sterling is driven primarily by relative US /UK interest rates. It is likely that US interest rates will continue to rise this year, but UK rates will not. March 29 is still a crucial factor. If the UK crashes out, sterling will fall, at a guess, to $1.10, but it should recover from this level to, say, $1.25 quickly, as speculative dollars flood into London.

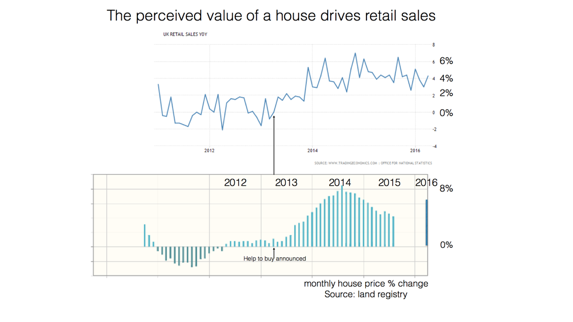

Taking all the above into account, a 1% growth in real wages can be expected. But this may not translate into higher real spend on retail. It will depend to a large extent on confidence, which in turn depends on Westminster, and perceived house prices.

Indicator 3: House Prices

The Land Registry indicates 2.8% growth in November, yoy. The Nationwide index for January showed a 0.1% increase, yoy. The Halifax 1.3% for December 2018, yoy

We await the December Land Registry data, but anecdotal evidence suggests the market has stalled. The Press made much of the worst case scenario when the Bank stress-tested UK banks, assuming a 33% fall in house prices. The Bank did not say this would happen. All the banks passed the stress test.

But would house prices collapse if there was a no deal Brexit? My guess is we would see a 10% fall in prices on average and a sharp drop in the volume of transactions. Assuming the withdrawal package is passed by Westminster, I guess the market would quickly recover, with an increase in transactions to 1.2m over a 12 month period, and average prices rising by 3%.

The next graph shows how quickly retail sales responded to rising house prices. This wealth effect kicked in after help-to-buy was announced. The British have more wealth tied up in housing than any other G7 country.

Central London, high end, speculative house prices are falling. But this is really of no consequence for our Economy. Many of the £5m-plus properties are bought for speculative gain, similar to cars and paintings. Prices at the £10m-plus end will fall by 20% before, no doubt, rising again.

For most purchasers, who are looking for a home, the price will depend on location. Property located near good public transport, good schools, a Waitrose (Booths in the North) and green space will always do better than average. Currently however, the market has stalled due to Brexit uncertainty. Assuming the withdrawal is agreed by 29 March then volumes will recover. One word of warning: UK mortgage lenders are expecting surveyors to value at up to 20% below market for the purposes of mortgage provision. This will give some would-be buyers a problem, unless the vendor accepts an offer below the market. At this stage of the economic cycle, anyone with high leverage (debt to equity ratio) is seen as risky by lenders. This also applies to house builders.

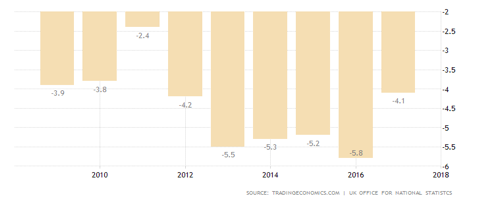

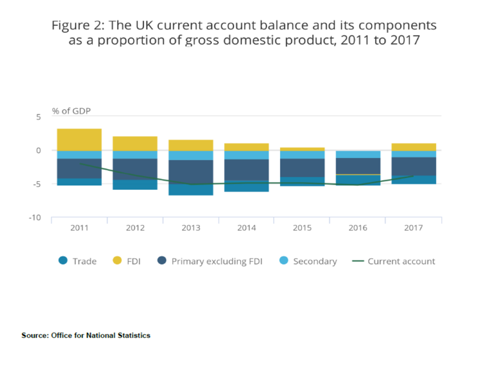

Indicator 4: the composition of the UK balance of payments

The UK runs a sizeable deficit with the rest of the World. The chart shows the current account as a % of GDP. This puts us into a group of deficit countries such as Turkey -4.5%, Pakistan -5.7%

Argentina -6% Columbia -3.2% USA -2.5%. The Euro-area members all run surpluses, except France and Greece. As a whole, the EU area runs a 3.5% surplus with the rest of the World. In essence, that means the UK is living beyond its means, or as Mark Carney put it, we survive due to the generosity of foreigners. This deficit has to be financed.

The second chart shows that in 2016, net FDI (Foreign Direct Investment) made no contribution to financing our trading deficit. In 2017, devaluation resulted in a net surplus. A no deal exit would boost FDI as the UK became bargain basement, thanks to the devaluation of sterling. This would involve the purchase of equities, bonds, and cash. But long-term job creating inward investment is likely to fall off a cliff under WTO rules. We must remember that for a US and Japanese company, the UK has been the first choice country to obtain tariff free access to the EU single market. Sony and Panasonic are moving their EU headquarters to EU countries. Nissan has halted plans to invest in Sunderland (not due to Brexit)

In my opinion the current account deficit and its financing is the elephant in the room. Leaving the EU will make it more difficult to grow our exports of goods and services to the EU. And it will reduce productivity enhancing FDI. We have already promised the EU we will not use the taxation system to attract investors.

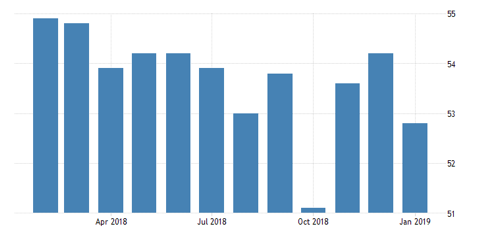

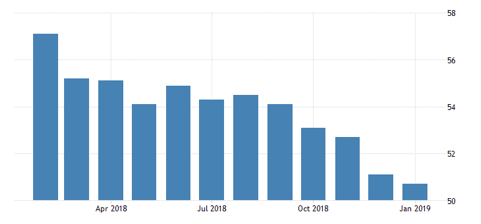

Indicator 5: The Purchasing Managers Index for Manufacturing

Any number above 50 suggests expansion. The chart below shows positive growth, but for reasons of fear of a hard Brexit.

K PMI for Manufacturing

Manufacturers are busy. This is because of stock building in case of a no deal Brexit. Stock building is the largest since the survey began 30 years ago. The issue for the economy as a whole is simple. If the withdrawal agreement is accepted, there will line of sight for at least two years. Final sales are unlikely to take off, so many companies will have excess stock. De-stocking will follow, and production volumes consequently fall. Paradoxically, success in getting a withdrawal agreement through Parliament could trigger a recession.

The latest Deloitte survey of UK Chief Financial Officers shows that uncertainty is driving a shift towards defensive strategies among British businesses. The UK’s growth prospects are significantly dependent on deal or no deal. Corporates are cutting back on capital expenditure and hiring. Cost reduction is the top priority for CFOs. The last time they did this was 2010.

CFOs continue to be pessimistic about the long-term effects of Brexit, with more than three-quarters expecting it to lead to a deterioration in the business environment. Domestic risks seem to be the dominant concern for CFOs, followed by greater US protectionism and weak demand in the UK. Despite slowing global growth leading to a weaker external environment, CFOs rate emerging market and euro area weakness among the bottom three risks to their businesses.

After a long period of easy access to cheap credit, funding conditions have begun to tighten. CFOs report that the cost of credit for their businesses has risen to its highest level in almost six years and availability has dropped to a two-year low. Rising interest rates have also brought a renewed focus on corporate leverage. For the first time in eight years, a net balance of CFOs rate UK corporate balance sheets as over-leveraged.

The survey reveals a divergence of opinion between economists and CFOs on the likely nature of Brexit. The latest consensus growth forecasts suggest that economists expect a transition deal, but corporates are positioned for the hardest Brexit, with risk appetite at recessionary levels and an intense focus on cost control. Businesses seem to be increasingly pricing in a worst-case outcome. Anything better, including a delay or a deal, could deliver a Brexit bounce in sentiment.

Conclusion for the UK

Unless money supply and or confidence picks up, the second half of 2019 and into 2020 will proves challenging. A successful withdrawal deal will improve confidence and this may prevent a recession, unless excess stocks are reduced by cutting output. But do not expect real GDP to be better than 1.3% this year.

A no-deal Brexit will cause a recession as supply chains are disrupted and WTO tariffs applied to our exports to the EU. It is likely that inflation will quickly rise to 4% (as sterling drops) and wages will not keep up. The Bank of England will raise interest rates in order to finance our trade deficit .

House prices on average will fall 10% further depressing consumer confidence. And there is likely to be political turmoil with the prospect of an election and, possibly, a win for the Labour party (although Corbyn is out of line with his rank and file and is showing none of the attributes needed by a leader)

But a weak currency will attract more overseas visitors, London retail, hotels, and hospitality will benefit, as will share prices and if sterling drops far enough, high end house prices (although the threat of a Labour Government might offset the devaluation stimulus.)

At this time, I am unable to make sensible forecasts, beyond that which I have written.

Readers of my ramblings will have already prepared their businesses for the next year. They will have built higher cash reserves, they will have revisited their strategies and made sure that all employees know, with absolute clarity, who they want as customers and why the business is distinctive and compelling for those customers.

After 29 March hopefully things will be clearer.

Now we will look at the EU

Money supply growth in the EU has softened a little over the past year but it is sufficient to

enable EU real GDP to grow at 2.5%, if the velocity of money doesn’t fall.

EU broad money growth year on year

The best indicators of velocity are the PMI index and retail sales.

The chart below is the composite PMI for the EU. It is disturbing, showing a rapid decline in confidence since August, led by German export-facing manufacturers.

However, EU retail sales are holding up reasonably well – the data for December will either confirm or deny this statement.

EU Retail sales YOY

The latest EU business confidence survey (January 2019) indicates that, although growth has reduced to just under 2%, confidence has not significantly deteriorated.

The data we have to date suggest that, although The EU has slowed down, it will avoid a recession. The overall growth of the EU will be significantly determined by the German consumer.

Unlike the Brits, Germans always save at least 10% of their after-tax income. German retail sales, as in all countries, are volatile, but on average, Germany needs at least 3-4% growth to offset reduced exports to Asia and Brexit UK. Given their preferences, this is unlikely.

China

The Press is full of the Chinese slow down from 7% to 6%. To get it in perspective this means the size of China’s economy will double in 12 years instead of 10.2 years!

Broad money is growing at 8%. If inflation stays below 2% and velocity doesn’t fall. then 6% growth for this year and next is a reliable forecast. Retail sales are still strong.

China Retail Sales YOY

It would appear that China is managing the transition from. 1.4 Bn pairs of hands to 1.4Bn brains.

I spent some time with a Chinese IT consultant based in LA. After two years in California she remarked how backward the US is compared to China on connectivity, convenience shopping, and Internet banking. However she intends to stay because she hugely valued freedom of thought and an open internet. A small piece of evidence that China is becoming a Global force.

It is likely that the attitude of Trump will speed this up.

The USA

US money supply growth has dropped from 6.5% pa to 4.3% per annum. This is why the Fed has held back the promised increase in interest rates. Like the UK, if money supply growth fails to pick up, we can expect a sharp USA slow down end of this year. With possible recession next year.

Retail sales data show the velocity of money has not picked up sufficiently to offset a reduction in money growth rate. It supports my forecast for lower growth middle end of this year.

US Retail Sales YOY

The US PMI

Overall View

The Global economy will slow down as we progress through 2019 into 2020. Recession or no recession will depend on confidence, which in turn depends on the quality of leadership in the major economies. There is not much comfort on this front as populism continues to produce new leaders who massively oversimplify the economic challenges the World faces.

However a US business owner expressed to me an optimistic view ‘Trump is the enema long overdue in the US economy’. Just possibly, Brexit will be the same for the UK, but I have my doubts.

Please remember the Global system exhibits second level chaos.

The next update will have my School Report for last year. Expect it in May.

Rmfagg@aol.com February 2019

Roger Martin-Fagg

Roger Martin-Fagg

Roger Martin-Fagg is an economist turned strategist.

A behavioural economist who focuses on behaviour and feedback loops which are largely absent from conventional models.

He began his career in the New Zealand Treasury, then moved into Airline Business Planning and teaching postgraduates all aspects of economics. He designed and ran the postgraduate diploma in Airline Management for British Airways before joining Henley Management College in 1987, where for 21 years he taught senior managers macroeconomics and strategy.

Roger is an independent teaching consultant. He has been external examiner to Bath University, worked with the Bank of England, three of the major UK clearing banks, advised a major London recording studio for 15 years, and regularly talks to SME owners in the UK and Europe about economic trends. He is a visiting fellow to Ashridge, Warwick and Henley business schools.

Roger is a practical researcher. He focuses on how the economy really works and on the links between FT100 reward systems, the behaviour of banks and economic instability. He also researches his clients trading environment as a necessary component of his teaching. His book

“Making Sense of the Economy” is in its fourth reprint.

He speaks at conferences around the world on the economic outlook and its impact on business. His quarterly Economic Update is sent to 1,200 SMEs.

Roger is one of over 70 experts that works with the Property Academy’s members. Want to find out more about the benefits of Property Academy membership and attend a free trial meeting?

Follow our social channels here: