The latest economic update from one of the best economic forecasters in the UK, Roger Martin Fagg.

The latest economic update from one of the best economic forecasters in the UK, Roger Martin Fagg.

Many of Property Academy’s Members have had the experience of working directly with Roger in our mastermind group meetings and all our members receive his regular economic briefings.

Roger called the last shock General Election result and accurately predicted that Trump would be President months before anyone else. You can find more information about Roger, the many other benefits of Property Academy membership and apply to attend a Mastermind Group session at the bottom of this update.

In addition to his usual summary of world events, in this update, Roger writes a very honest personal ‘school report’ – comparing his recent predictions against actual performance. He may not always be right, but in the words of famous British Economist John Maynard Keynes, “It’s better to be roughly right than precisely wrong” and Roger is certainly top of his class.

This update only focusses on the UK.

At last it is now possible to map out the the UK economic landscape mostly thanks to those traditional labour voters who switched to Boris. I am assuming Boris will deliver on his core promise which is to be a one nation Conservative. He has promised new Tory voters that their trust in him will be justified.

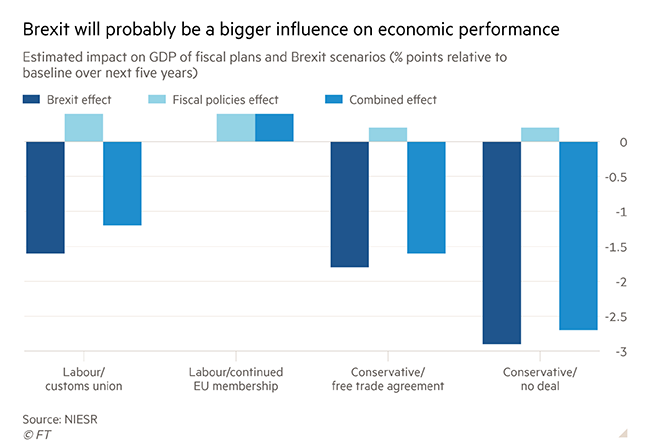

He will have to ensure the softest Brexit possible. In fact if jobs are to be protected and the tax base robust enough to generate the revenue to invest in education, health, training, and infrastructure, the UK will have to remain in the EU in all but name. The modelling by NIESR shows that a free trade agreement with the EU plus the tax changes will still result in GDP being 1.5% less than it would otherwise be in each of the next five years. This amounts to revenue, based on the current tax structure, being around £15Bn less each year than it would otherwise have been. To be fair if Savid Javid borrows and spends an extra £20bn each year then the net effect is £5Bn which is 1p on the basic rate of income tax. I do want to emphasise these are estimates and the outturn could be much better or worse than this.

The benefits of infrastructure spend take time to come through and it is reasonable to suggest that the incomes multiplier and productivity gains will not come through until 2022. But there are lots of private sector projects which will be commenced.

Between now and then Savid will have borrowed £60 Bn assuming he delivers on the promise.

It is reasonable to assume that this increase in borrowing will increase long run interest rates. Unless they can persuade the new Governor of the Bank of England to montetise the new debt via QE. or show overseas investors that UK debt is preferable to German or American debt.

Many of my leaver friends tell me that the Boris victory and getting Brexit done will unleash a torrent of productivity enhancing inward investment. New trade deals with the growth economies in the World and the USA will create an economic boom. GDP will grow more strongly than is suggested by the likes of me. I remain to be convinced. It would be fantastic (to coin a much used word recently!) if I was totally wrong.

Meanwhile.

The Government is merely planning to redistribute taxpayers money. The economic growth impact will come from the £20Bn of borrowed money being invested in capital projects supported by the private sector splashing the cash!

During the election there was a clear statement that net immigration will be brought down using an Australian type of points system. We will need increased labour supply to deliver new projects. The vote has given business some certainty. And it is likely that in 2020 a good many investment buttons will be pushed. Private sector spend will be financed by a combination of retained profits, share issuance and borrowing from the banking system. The first two increase the velocity of money the latter also increases the volume of money.

At this point we need to consider the impact of the new Government on inflation.

Currently our economy has very little spare capacity due to 3 years of underinvestment.

A wall of new money will mostly drive prices up in the short run. I expect inflation to be 3% and rising by this time next year.

As many of my regular readers know I believe that the growth rate of the money supply is a key driver of economic activity and if resources are scarce, the inflation rate.

2020 will be a good year, the current growth in money supply will increase and an 80 seat majority will give confidence resulting in increased velocity. I forecast real GDP will hit 2.2% by the end of 2020 but the new Governor of the Bank of England will be warning that interest rates need to rise as the inflation rate unexpectedly grows above 3%.

The key driver: money supply

The money supply in October grew at 3.7%. This is close to the 4% we need for steady real growth at 2%. Following the election result I expect to see 5% growth on money supply in the first quarter of 2020. This will finance a 2.2% growth in GDP with an inflation rate of 2.8%.

The time it takes for new money to flow through the whole economy varies with the level of confidence: it can take up to two years. But I expect a significant upturn in velocity. The best indicator will be monthly house sales. They are normally around 100,000 per month: we can expect 110,000 per month by April assuming the weather is normal for the time of year.

There will price recoveries in London and the SE and average selling prices will rise by 5% across the country.

The construction sector will be inundated by much needed new work as the capex buttons are pressed by finance directors. Banks will become more willing to lend. The so called Boris Bounce will happen.

What could possibly go wrong?

The key to a continued expansion is how the UK Government chooses to manage its relations with the EU.

If there is a cabinet reshuffle during which members of the ERG are demoted it will be a clear sign that Boris wants a soft Brexit. He will need this if he is to deliver his promise to the North. If we continue to match EU standards, recognise how important the EU market for services exports and promise to regulate financial services at EU standards then I anticipate a free trade deal on goods will be struck within 18 months and for our financial services sector equivalence will be granted. In most respects this will be business as usual.

However if there is a move towards creating Singapore on Thames and a pivot to the USA then the Boris Bounce will deflate by the end of next year. My instinct is this will not happen. For example the race to the bottom on Corporation Tax will not happen. Hopefully the ERG will become a knitting club in the House of Commons and fade into oblivion.

The February or March budget will give some clear messages of the intended path which I expect to be old fashioned one nation Toryism which is defined as paternalistic approach recognising that society develops organically and Government should support change but not engineer it.

In conclusion

2020 will be a good year.

Real GDP up 2.2% by year end, wage growth 4%, house price growth 5%, interest rates no change until November then a small uplift to 1%.

Retail will enjoy more consistent monthly demand with volumes growing 3% and value 5%.

CPI inflation will creep up towards 3% by the end of the year.

Sterling/dollar between $1.30 and $1.40

Sterling /Euro 1.20

I will comment on the rest of the World in my next update which should be out just after the budget. I wish you and those you love and respect a really Happy Christmas and for a change there will genuinely be a prosperous 2020!

PS I am not always a miserable B…………r!

Rmfagg@aol.com Prepared December 15 2019

Roger Martin-Fagg

Roger Martin-Fagg

Roger Martin-Fagg is an economist turned strategist.

A behavioural economist who focuses on behaviour and feedback loops which are largely absent from conventional models.

He began his career in the New Zealand Treasury, then moved into Airline Business Planning and teaching postgraduates all aspects of economics. He designed and ran the postgraduate diploma in Airline Management for British Airways before joining Henley Management College in 1987, where for 21 years he taught senior managers macroeconomics and strategy.

Roger is an independent teaching consultant. He has been external examiner to Bath University, worked with the Bank of England, three of the major UK clearing banks, advised a major London recording studio for 15 years, and regularly talks to SME owners in the UK and Europe about economic trends. He is a visiting fellow to Ashridge, Warwick and Henley business schools.

Roger is a practical researcher. He focuses on how the economy really works and on the links between FT100 reward systems, the behaviour of banks and economic instability. He also researches his clients trading environment as a necessary component of his teaching. His book

“Making Sense of the Economy” is in its fourth reprint.

He speaks at conferences around the world on the economic outlook and its impact on business. His quarterly Economic Update is sent to 1,200 SMEs.

Roger is one of over 70 experts that works with the Property Academy’s members. Want to find out more about the benefits of Property Academy membership and attend a free trial meeting?

Follow our social channels here: