The latest economic update from one of the best economic forecasters in the UK, Roger Martin Fagg.

The latest economic update from one of the best economic forecasters in the UK, Roger Martin Fagg.

Many of Property Academy’s Members have had the experience of working directly with Roger in our mastermind group meetings and all our members receive his regular economic briefings.

Roger called the last shock General Election result and accurately predicted that Trump would be President months before anyone else. You can find more information about Roger, the many other benefits of Property Academy membership and apply to attend a Mastermind Group session at the bottom of this update.

In addition to his usual summary of world events, in this update, Roger writes a very honest personal ‘school report’ – comparing his recent predictions against actual performance. He may not always be right, but in the words of famous British Economist John Maynard Keynes, “It’s better to be roughly right than precisely wrong” and Roger is certainly top of his class.

Only three months ago I gave evidence that we were close to the top of the cycle. I am now worried that the current combination of global events could create a perfect storm. Brexit is a side show but it increases the risk the the UK economy.

Donald Trump apparently has a degree in economics but this could be a fake Wikipedia entry! He should have learned three things. Firstly an economy is characterised by strongly positive feedback: a small change in one part of the system is magnified as other parts of the system react. Positive feedback is the mechanism which magnifies small changes to create boom and bust.

Secondly the so called Prisoners Dilemma: a theory which shows why two completely rational individuals might not cooperate, even if it appears that it is in their best interests to do so. In trade it always pays to cooperate, no one wins a trade war.

And thirdly the role of the federal reserve is to ensure that inflationary expectations do not take off by raising interest rates in a timely fashion.

As I write there is a number of activities in the Global system which in the next 12 months could combine to create a perfect storm. A perfect storm is an event in which a rare combination of circumstances drastically aggravates the event.

Here are the circumstances:

Due to USA sanctions on Iran (and a faster than expected global growth rate) the oil price has doubled in the last year. US tax cuts are causing the US economy to overheat: registered unemployed now 3.9% (the same as the UK). The US inflation rate is now 2.9%. The most recent real growth rate is 4.1%. This is well above the long run average growth rate of 3.2%.The response of the Federal Reserve will be to continue raising interest rates.Historically a 1% increase in the fed funds rate reduces real GDP growth by 0.7%.

However given the scale of the fiscal stimulus (an extra $1.2 trillion dollars over the next five years), the impact of interest rates on growth may be lower. The implication being that they will have to be raised by more than expected.

A 1% increase in US rates lowers emerging market (EM) economies growth by 0.8% .Brazil, Chile, China ,Colombia, Czech Republic, Egypt, Greece, Hungary, India, Indonesia, Korea, Malaysia, Mexico, Morocco, Qatar, Peru, Philippines, Poland, Russia, South Africa, South Korea, Taiwan, Thailand, Turkey and United Arab Emirates.

Source:

Iacoviello, Matteo and Gaston Navarro (2018). Foreign Effects of Higher U.S. Interest Rates. International Finance Discussion

EM countries typically run a current account deficit so they rely on foreign capital inflow to fund those deficits. In order to attract that foreign capital inflow, they offer high interest rates. When U.S. interest rates were low, the so-called ‘carry trade’ (the practice of investors borrowing cheap U.S. money and investing it in these higher-yielding currencies) supported the EM world.

Last year, the weak dollar also helped those EM economies. But as the interest rate differential between the dollar and emerging market currencies narrows, the latter become less attractive, discouraging investors from taking on the investment risk. With increasing currency volatilities in emerging markets, that is sending capital back into the dollar.

This poses a threat to the EM countries. Their economies grow by leveraging, but not only is that foreign money not coming in, their foreign borrowing levels – primarily denominated in U.S. dollars – are surging as a result of the stronger dollar and higher U.S. interest rates.

To illustrate this phenomenon, since the beginning of this year, the Turkish lira has dropped by 20 percent and the Brazilian real by 11 percent. The South African rand and Russian ruble seem equally vulnerable.

Although not an emerging market economy, the UK has to attract around £80Bn of foreign capital each year to finance its current account deficit. If the Bank of England fails to raise UK interest rates then we will see a weaker pound especially against the dollar.

The Threat of Trade Wars.

We are beginning to understand Trumps approach: he threatens and then climbs down. However the threat has a material impact: it causes uncertainty and corporates to conserve cash. China has just announced a reduction in required reserve ratios for banks and a fiscal stimulus to offset the slowdown which began following Trumps announcement of tariffs.

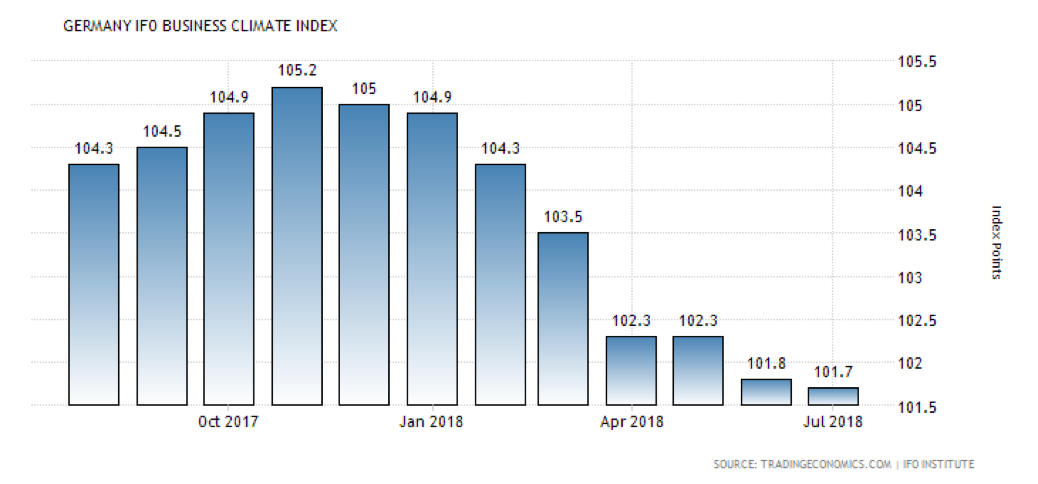

Last week we saw Juncker on the steps of the White House apparently having influenced Trump not to impose tariffs on EU produced cars. It is probable that the EU threat of tariffs on $400Bn of US exports had an impact! But meanwhile M-B and BMW issue profits warnings and their shares loose 10% of value. And the key German IFO index which surveys 7000 businesses across all sectors shows a significant softening of confidence

Brexit

It is unclear if the EU will agree to the UK’s proposed withdrawal conditions. The UK has created a brilliant fudge which the EU can see through.The European parliament threatened to veto any agreement if the UK did not do more prevent a hard border with Ireland after it leaves the bloc. And to date they do not accept that a third country (the UK) should be allowed to collect tariffs on goods imported to the UK and then exported to the EU. Both parties are preparing for a no deal situation. And as at July 30th this looks the most likely outcome.

The expectation of a no deal has more impact than the event itself (if it happens). The latest survey of CFO’s in the UK shows they are taking a much more cautious approach to the future. In particular they are increasing their cash balances. It has to be stated yet again: when corporates run for cash SME’s suffer. In addition UK banks are tightening their lending criteria. The impact is a reduction in the velocity of money, lower than expected sales, and a slow down or at worst a recession.

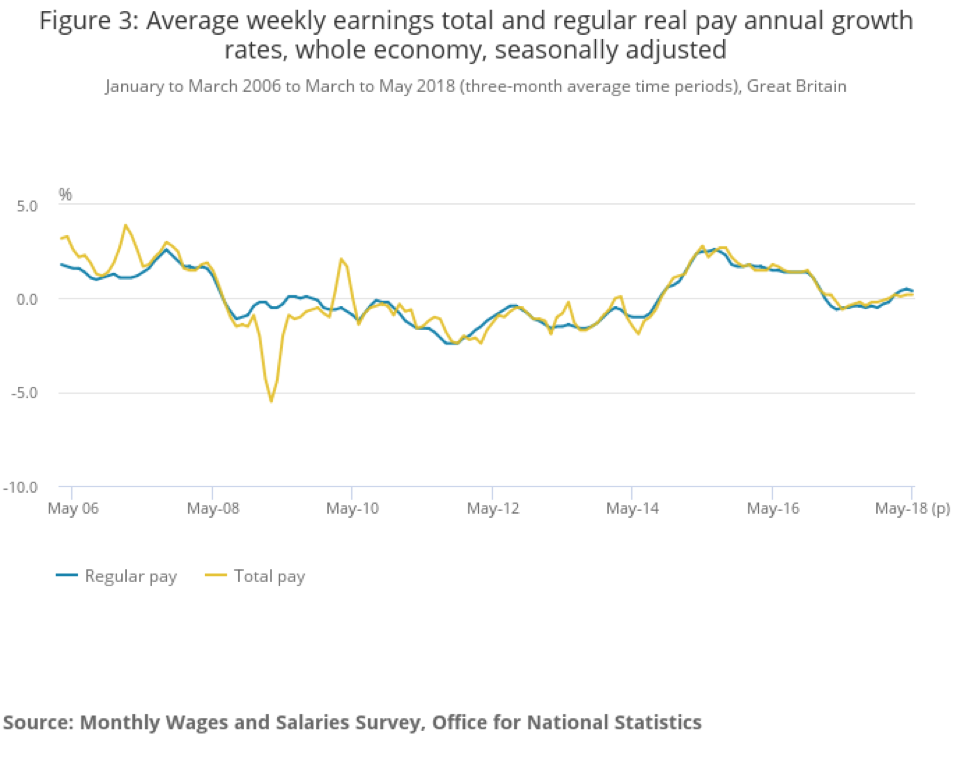

Since the Nation voted leave 18 months ago, exports to a booming global economy offset the sluggish growth in domestic demand. Thanks to Mr Trump the global economy is slowing and the offset for UK growth is weakened. Real pay is only just growing.

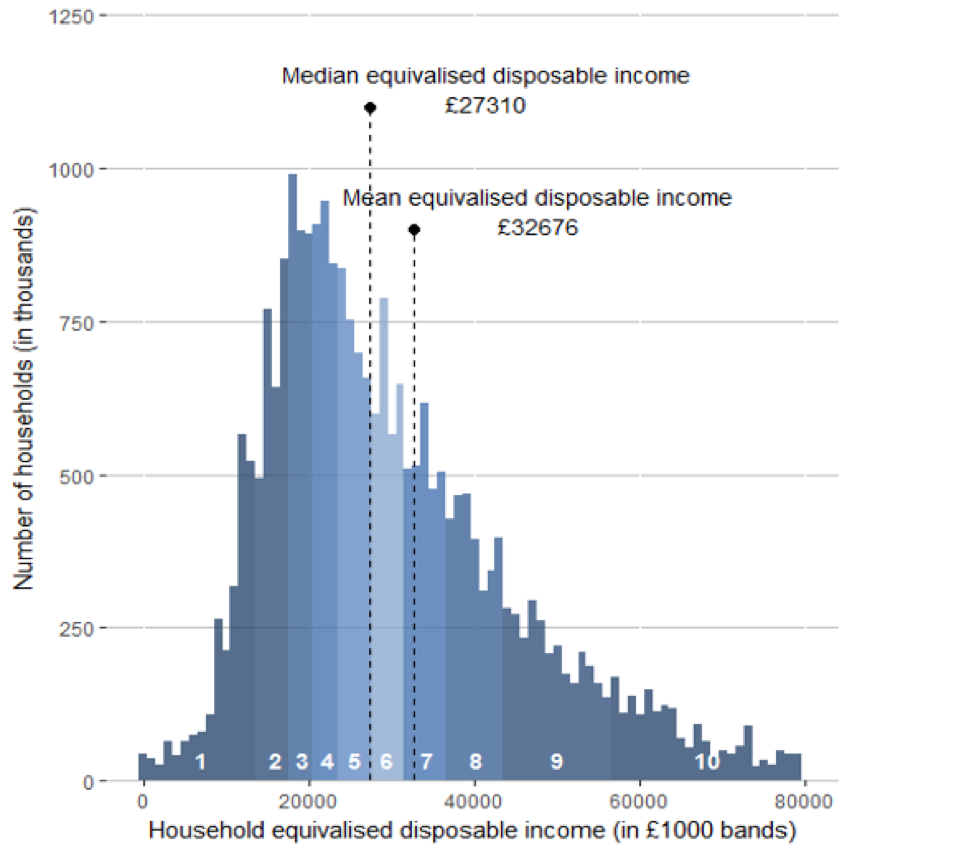

If we look at the distribution of disposable income we can see most UK households live on less than 30k a year after tax. Since the vote to leave there has been no improvement in real incomes for the majority.

Source:ONS

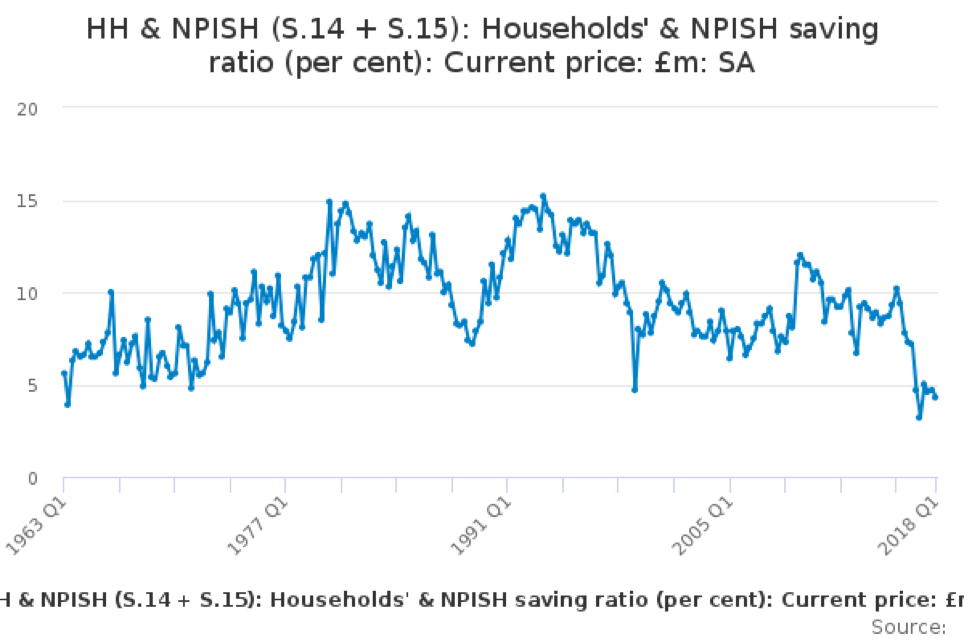

Households have reduced their savings rate and increased their debt to maintain consumption. In 2017 they spent £25Bn more than they earned (it averages out at £900 per household).The poorest 10% of households spent two and a half times their disposable income, on average, in the financial year ending 2017. The richest 10% spent less than half of their available income during the same period.The ONS found that the deficit among UK households, equivalent to 1.2% of GDP, contrasted with a surplus in France equivalent to 2.7% of GDP and a surplus equivalent to 5.1% in Germany.The ONS said households took out nearly £80bn in loans in 2017, the most in a decade. But they deposited just £37bn with UK banks. Banks must be balancing their book by accepting business deposits and or borrowing short term in the wholesale market. You will recall the crash in Q3 2008: the wholesale market ran out of money due to a lack of trust in the London market. Could a no deal Brexit do the same again?

This all points to an economy which is vulnerable to small and unplanned events and households who have little in the way of cash reserves if there are layoffs or less hours of work required.

NOS

NPISH is non-profit institutions serving households

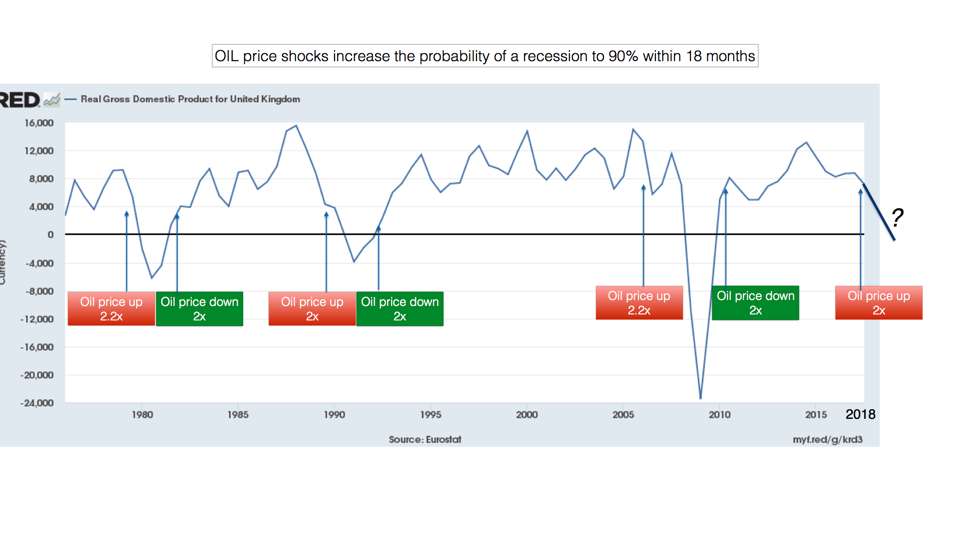

The Price of Oil

The graph below shows than when the price of oil doubles a recession follows within 18 months. The exception was 2005. A doubling in the price of oil sucks spending power out of oil importing countries, it ends up in oil exporting countries who do not spend it immediately: the global velocity of money drops sharply. In 2005 oil went up 2.2X but households maintained their spending using credit.

This time around they are mostly maxed out and banks have already tightened their credit terms. Hence the possibility of a recession a year from now.

In Summary

A boom in the USA requires significantly higher interest rates. The USA sets the level for the World. Emerging markets face much higher interest rates or a collapsing currency. The doubling in the price of oil squeezes household discretionary income. UK households are particularly vulnerable. Fearful finance directors conserve cash so smaller companies are not paid on time. Existing money works less hard and new money does not expand sufficiently to offset this. The result is an unplanned drop in sales in all sectors except those supplying the oil and gas industry. A sharp slow down possibly followed by a recession. For the UK the Brexit uncertainty just increases the chance of a recession in the next 18 months.

As the Western World heads for the beach and the mountains we can hope for some respite. When people return to their desks in September, refreshed, and able to think more strategically I would hope the threat of a hard Brexit and Trump trade wars diminishes and yet again I will be proved wrong!

Have a restful holiday.

Rmfagg@aol.com July 30 2018

Roger Martin-Fagg

Roger Martin-Fagg

Roger Martin-Fagg is an economist turned strategist.

A behavioural economist who focuses on behaviour and feedback loops which are largely absent from conventional models.

He began his career in the New Zealand Treasury, then moved into Airline Business Planning and teaching postgraduates all aspects of economics. He designed and ran the postgraduate diploma in Airline Management for British Airways before joining Henley Management College in 1987, where for 21 years he taught senior managers macroeconomics and strategy.

Roger is an independent teaching consultant. He has been external examiner to Bath University, worked with the Bank of England, three of the major UK clearing banks, advised a major London recording studio for 15 years, and regularly talks to SME owners in the UK and Europe about economic trends. He is a visiting fellow to Ashridge, Warwick and Henley business schools.

Roger is a practical researcher. He focuses on how the economy really works and on the links between FT100 reward systems, the behaviour of banks and economic instability. He also researches his clients trading environment as a necessary component of his teaching. His book

“Making Sense of the Economy” is in its fourth reprint.

He speaks at conferences around the world on the economic outlook and its impact on business. His quarterly Economic Update is sent to 1,200 SMEs.

Roger is one of over 70 experts that works with the Property Academy’s members. Want to find out more about the benefits of Property Academy membership and attend a free trial meeting?

Follow our social channels here: