By Roger Martin-Fagg

Since my last update a great deal has happened:

Since my last update a great deal has happened:

– Otmar Issing, the principal architect of the Euro, has stated that the Euro is bound

to fail and that Greece should have left the system in 2010.

– The British Government is beginning to realise that a clean break from Europe is

impossible without doing long term damage, and that a transitional arrangement

must be put in place as soon as possible.

– Jean-Claude Juncker is on record stating that ‘we need less interference from

Brussels when it comes to the things that Member States can deal with better on

their own. That is why we no longer regulate oil cans or showerheads, but

concentrate instead on what we can do better together rather than alone’.

– Near zero interest rates have done virtually nothing to stimulate investment in

productive capacity. The UK Treasury is dusting off the Keynesian model which

emphasises infrastructure spending as a route to higher productivity. But long run

interest rates are rising.

– The UK construction industry will need to recruit 700,000 people over the next 5

years to replace those leaving the industry, mostly through retirement. Currently

13% of the workforce is from overseas, 25% of whom are in London.

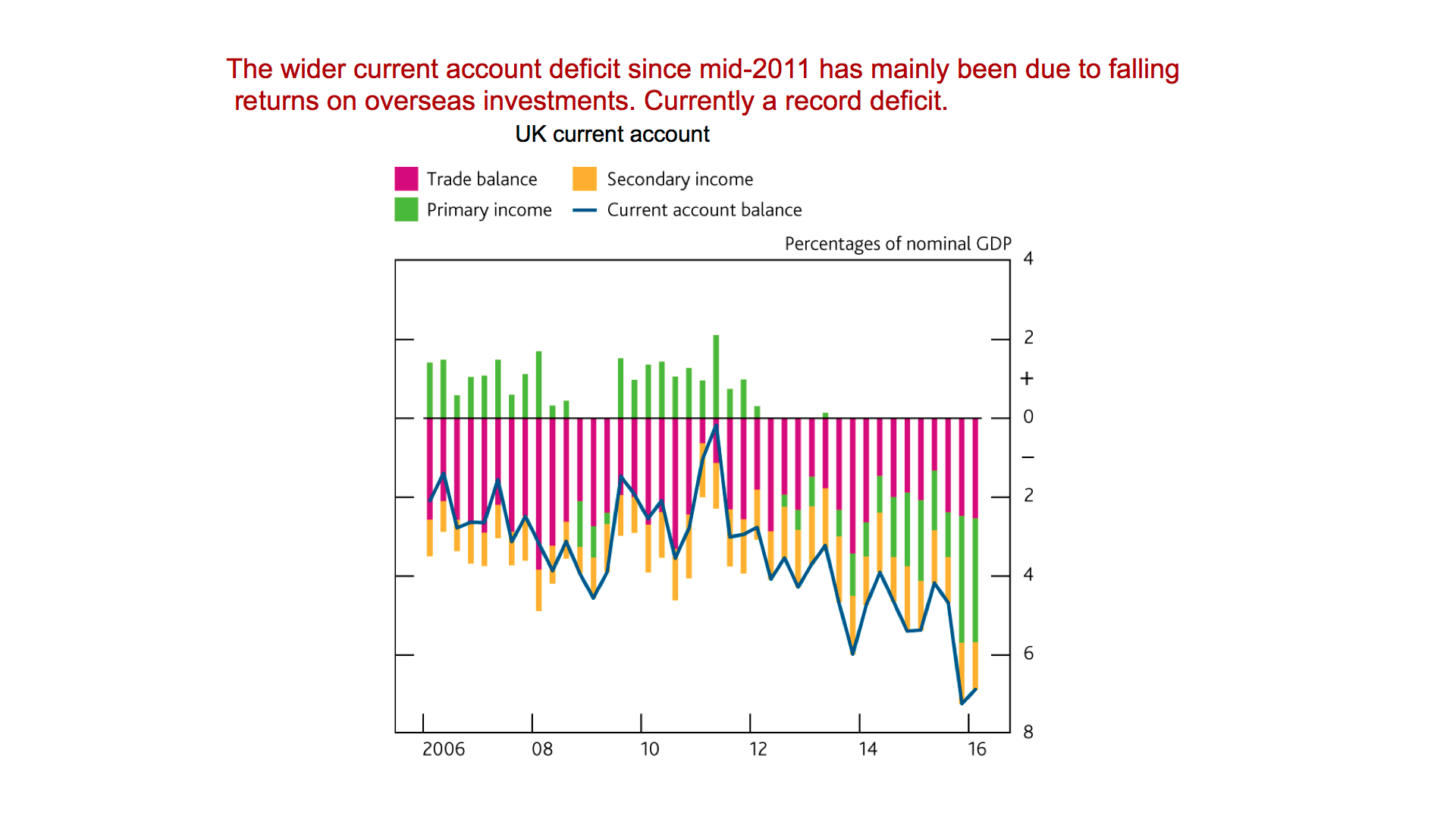

– Sterling has lost 16% of its value since the referendum. The UK balance of

payments deficit is a record 7% of GDP.

– Donald Trump could be the next President of the USA and Commander-in-Chief.

– A successful SME corporate travel company has noticed more business travel to

countries further afield in recent weeks.

– The Bank of England expects inflation to be 3% by the end of 2017, but Mark

Carney has said they will tolerate overshoot on the 2% target. This implies a

delayed interest rate hike, but no further cuts. Normally base rate is inflation plus

2.5%, but we are not in normal times!

The Brexit Vote

The British seem to be preoccupied with their own point of view without reference to the

views of our trading partners of the past 40 years.

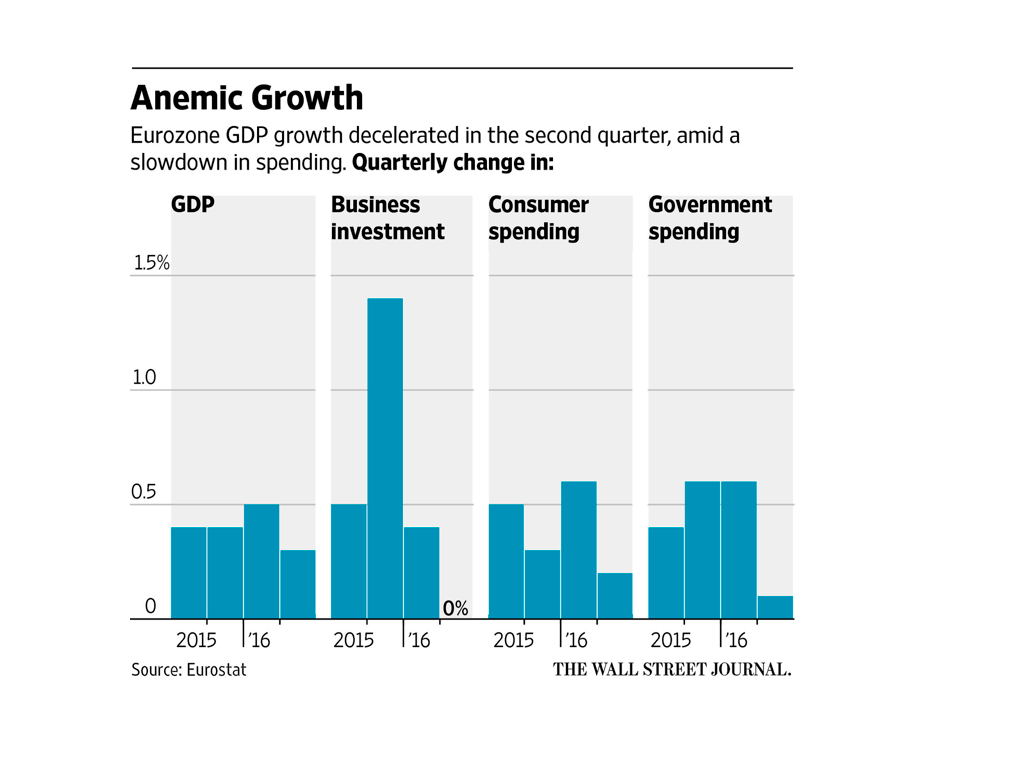

The run up to the vote clearly depressed confidence for business in the EU, and the

outcome seems to have reduced EU retail sales. One must assume EU consumers are

reflecting on the possibility of changes in their own country.

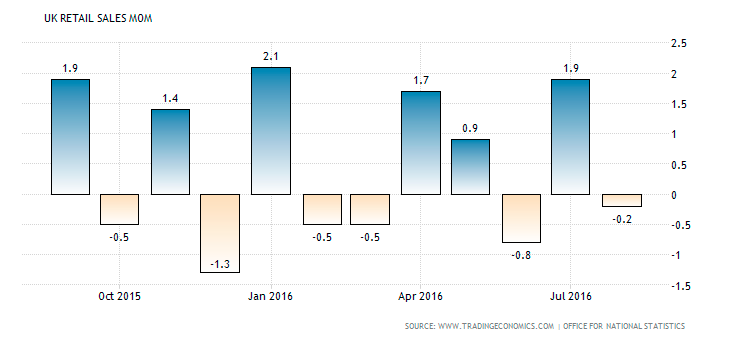

Meanwhile the British carry on shopping, with retail spend in September up 1.6%.These

figures are inflation adjusted.

There can be no doubt that the British vote has encouraged the many within the EU who

share similar views, and there is growing evidence that Brussels is beginning to modify its

stance.

‘we need less interference from Brussels when it comes to the things that Member States

can deal with better on their own. That is why we no longer regulate oil cans or

showerheads, but concentrate instead on what we can do better together rather than

alone’.

Juncker September 2016

And Professor Otmar Issing writing in the Central Banking magazine is convinced the Euro

project is on the slippery road to collapse. This is notable as Otmar was the chief architect

of the system. He is clear that “structural incoherence” has been disguised by cheap oil,

quantitative easing, profligate public spending and a cheaper Euro. He suggests that the

next downturn will be the big test. Greater political fatigue, high levels of debt, and

significant unemployment could mark the end of the Euro, he says.

He believes the ECB is in an untenable position because it holds a trillion euro bonds on

its balance sheet, many of which were bought at artificially high prices, and will rapidly

become almost valueless in the next downturn.

These remarks suggest to me that some of the institutions of the EU are being increasingly

recognised as not fit for purpose by those who work in them. What does this mean for the

UK?

After Germany we are the biggest net contributor to the EU budget. In 2015 our net

contribution was £9Bn, our gross contribution was £13Bn.

The EU budget is under severe pressure. When we leave, they will need to find at least

£9Bn from other members. The UK, Germany, France, and Italy together provide over

60% of the funding.

The EU needs our money. We need to control immigration (the will of the people). We

need to maintain free access for financial services (last year we made a surplus of £21Bn

on sales to the EU), for manufacturers, for travel, for holiday homes, etc.

The deal for Norway and Switzerland was meant to be transitory, but has become

permanent.

We need to do a transitory deal as follows:

We pay £ 13Bn per year, we get no farm support or regional aid back. We are free to limit

migration. We only have accept EU law in so far as it affects trading standards. We have

no seat at the table. But our access to the market remains as it is today. It is clean, costed

and simple.

So how do we sell it to the leavers?

It would cost £3.84 per person per week- or one Starbucks latte.

Of course we would probably have to keep regional aid and farm support going, which is

another say £5Bn of cost, 1p on the basic rate of tax.

But for £3.84 a week we save a fortune in lawyers and trade negotiators, we get our

sovereignty back from Brussels (we never lost it, but Boris would have to declare it). And if

the EU does collapse we are not part of it.

Meanwhile the EU is busy saving itself, so this transitory arrangement becomes

permanent.

If I have understood the leavers arguments correctly, they are not opposed to trading with

the EU, but they dislike the loss of sovereignty, the bureaucracy (which is unaccountable

they say), and uncontrolled immigration (from the EU).

For £3.84 per week we can meet their requirements.

My instinct is that the EU would agree to such an arrangement. As the political mood shifts

within the EU there are clear signs that the free movement of labour is less attractive to the

EU electorate. Many years of prolonged negotiations with Britain when resources are

limited and there are much bigger issues on the agenda could be viewed as a distraction.

What is the alternative?

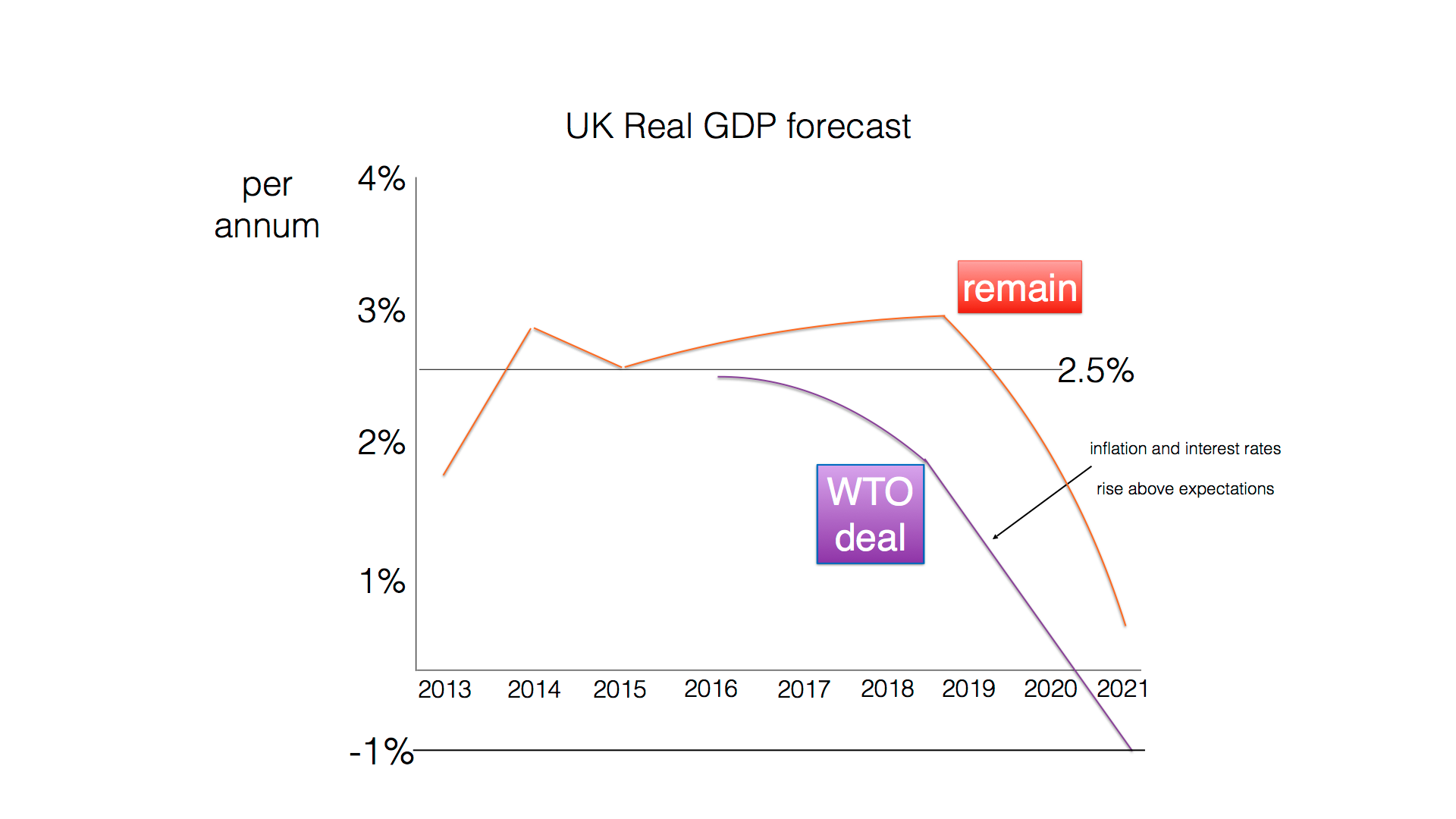

The so called hard Brexit.

We leave within the next three years and then revert to WTO rules to access the single

market. The current rules would kill the UK motor industry because of the 10% tariff. It

would take at least ten years of negotiation to tailor a motor industry package (which would

need to be agreed by 27 countries, so make that 15 years). Note that the EU-Canada deal

has been 7 years in the making, and Wallonia (the French speaking part of Southern

Belgium) has the power to stop it. As I write this, they intend to.

We would not be allowed to do tailored deals with each country within the EU, so each

prospective deal would require 27 countries to agree.

We would probably lose the inward investment from EU and USA companies (the USA has

£600Bn of investment in the UK). Our balance of payments current account deficit would

have to fall to a level which we could finance. This means a reduction from the current

£126Bn deficit per annum to around £35Bn. It is doubtful we could do this by raising

exports sufficiently, so we would have to reduce imports. This is usually achieved by a

recession: as the weak pound drives up inflation, wages fail to keep pace, and real

spending falls.

The WTO option would without doubt reduce the standard of living as real wages fell by

around 2% a year until a tailored deal was in place.

It would probably also wipe 10% or £600Bn of the value of UK houses in 2021-2023 as

interest rates go above 4% in order to finance the current account deficit.

A look ahead to the UK Autumn Statement

I am one of many who now think Quantitative Easing and near zero interest rates has

ceased to work apart from keeping share prices well above fair value and thus making the

rich richer. It is clear that the money supply in the West is now growing sufficiently to

maintain normal growth. But normal growth is below par because investment spending is

insufficient and productivity growth too low.

Keynes famously said ‘the colour of businessmen’s livers’ determines the investment

decision. And that is largely driven by confidence, which is in turn driven by expected

orders.

There are signs of a Keynesian mini revolution in the UK Treasury. Chancellor Hammond,

who used to be in the housing construction sector, has hinted at increases in Government

funded infrastructure spend.

Already announced is the release of £2bn of public land and £3bn of funding for small

house-builders. Both will increase the velocity of existing money and, to a small extent,

new housing will improve labour mobility.

We can expect more announcements in November. I guess the Treasury will be happy to

take the deficit up to £80Bn from the current £67Bn. This will be about 4% of GDP.

They will also announce measures to improve the supply of home-grown construction

workers, because as above a recent report suggests that over the next 5 years the sector

will need 700,000 new workers.

The USA

We wait with bated breath. I think Trump will just squeeze past Clinton and become the

next President. His pitch that she is a ‘crook’ and he is a savvy businessman resonates

with those in small town USA who choose to ignore his own illegal and morally repugnant

practices. He is clearly authentic, she is clearly not – or so the message goes. His

repeated challenge that she has had 30 years to get things done, but hasn’t managed to

change much, whereas he is a multi-billionaire because he gets things done is another

plus in so many eyes. He also struck home when he agreed he said many disgraceful and

unacceptable things about women, passed off as ‘locker room’ talk, but Bill Clinton acted

them out – this should bear no reflection on Hillary, but the world isn’t quite advanced

enough for that mindset. However, the majority of women in the US who were considering

voting for Trump have recently changed their minds (according to polls), given the number

of women who have come forward to accuse him of various grades of sexual harassment

and assault. He is currently 8 – 10 points behind, but Brexit showed us the fallible nature

of polls.

The entire process should be a plot in a scarcely credible dystopian novel rather than real

life – but that’s where we are, and it will be an extremely close election with possibly

serious ramifications for social order in the self-styled most powerful nation in the world.

In slightly more positive news, Obama has not managed to achieve a great deal because

of the US system of checks and balances – this will also apply to the next President.

The economic impact is very difficult to call. I suspect a short period of dollar weakness

which will not persist as the markets see who is appointed into key roles.

US business investment peaked a year ago; it could rebound if big tax cuts on business

are mooted.

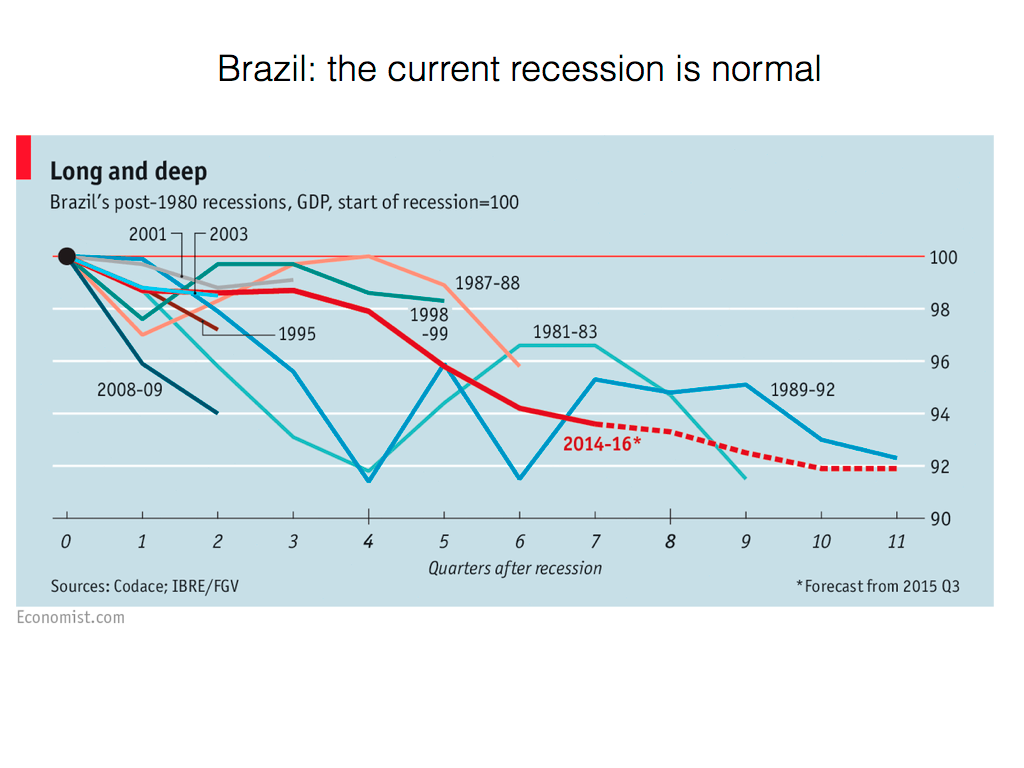

The BRICS

The leaders of Brazil, Russia, India, China and South Africa have just agreed to double

intra-BRICS trade by 2020.

Brazil and Russia are both in recession, China has stalled at 4% (according to electricity

demand), South Africa is flat. India is booming at 7.6% so I guess the rest want to sell

more to India.

The Outlook

I was impressed by a UK entrepreneur who said the other day he was visiting a trade

show in the USA. He hadn’t been for a number of years and previously he went to buy, but

this time it is to sell.

There is evidence that business travel is picking up and to places further afield.

This suggests to me that there is a spark of get up and go which, given the positive

feedback loop our economy always experiences, will result in growth better than forecast

by the majority for the next two years. Beyond that it is too early to tell, but I confess to

being one of those so called experts who is pessimistic for our growth prospects if we

pursue the WTO option.

Forecast to the end of the year

No change in base rate but long run interest rates will drift upwards as inflationary

expectations rise. This will increase mortgage rates but not until next year. If you can get a

5 year fix, do it now!

Core inflation up from 1.5% to 1.9%

£-$ 1.20 average

£-€1.12

If the Government makes it clear they are going for a soft Brexit to preserve current access

then the pound will be 5% stronger than the above figures.

Expansionary budget in November, with an announcement that we will look for

a transitionary deal with the EU.

Third and final quarter GDP growth will be 0.4% and 0.5% respectively.

House prices should slow their rate of growth from the current reported 8% year on year

(which I find difficult to believe) to 3-5%

Rmfagg@aol.com

18 October 2016